New York income tax is a crucial aspect of financial planning for residents across the state. Whether you're a long-time resident or new to the Empire State, understanding how this tax works can significantly impact your financial health. New York operates with a progressive tax system, meaning the more you earn, the higher the percentage of your income is taxed. This system ensures that individuals contribute according to their ability to pay, fostering a fair and equitable tax environment. However, navigating the intricacies of New York's tax laws can be challenging without proper guidance.

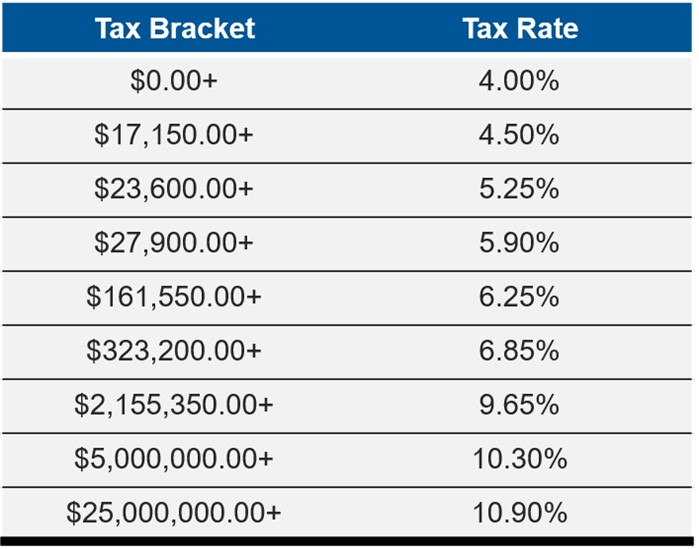

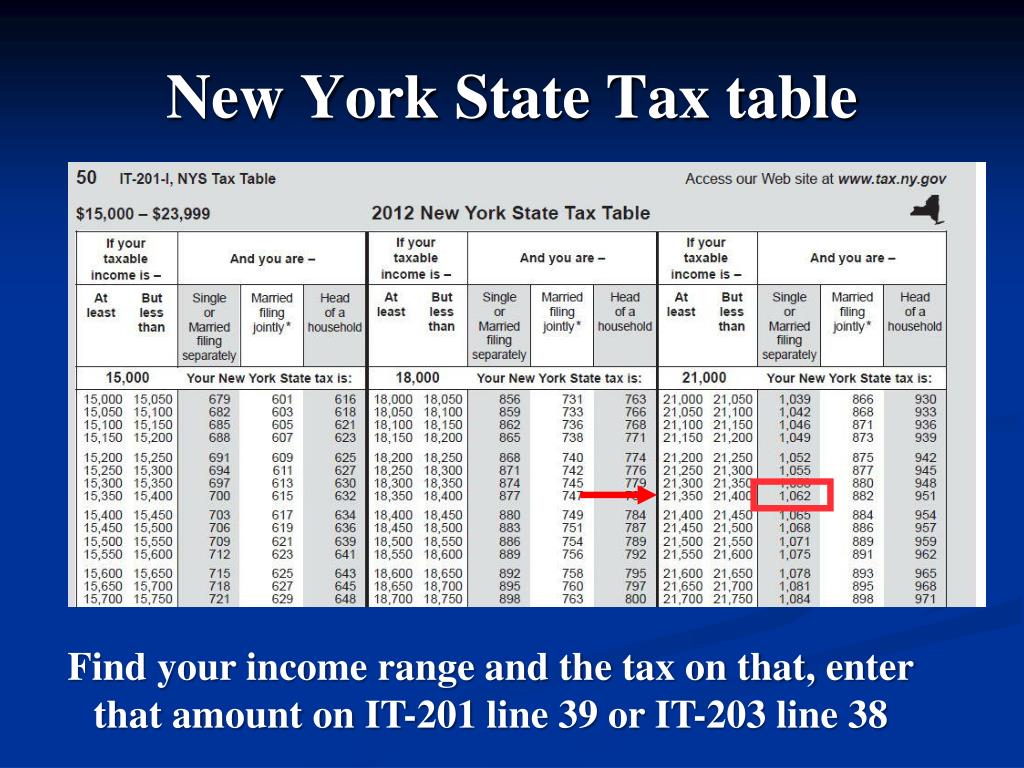

As of 2023, New York state income tax rates range from 4% to 10.9%, depending on your income bracket. These rates are subject to change based on legislative updates and economic conditions. Additionally, New York City imposes its own income tax, adding another layer of complexity for city dwellers. For instance, if you live in Manhattan, you'll need to calculate both your state and city income taxes. It's essential to stay informed about these tax obligations to avoid penalties and ensure compliance with state regulations.

Understanding New York income tax involves more than just knowing the rates. It requires familiarity with deductions, credits, exemptions, and filing deadlines. The good news is that the state offers several resources to help taxpayers navigate the process. From online calculators to professional tax advisors, there are plenty of tools available to simplify your tax obligations. This article will delve into the details of New York income tax, providing you with the knowledge and tools necessary to make informed decisions about your finances.

Read also:Will Arnett Alessandra Brawn Split A Comprehensive Look Into Their Relationship Journey

Table of Contents

- 1. What Are the Key Features of New York Income Tax?

- 2. How Does New York Income Tax Affect Different Income Brackets?

- 3. Why Is New York Income Tax Important for Residents?

- 4. How Can You Reduce Your New York Income Tax Liability?

- 5. What Are the Common Mistakes to Avoid When Filing New York Income Tax?

- 6. Frequently Asked Questions About New York Income Tax

- 7. Is New York Income Tax Fair for All Taxpayers?

- 8. How Do New York Income Tax Rates Compare to Other States?

What Are the Key Features of New York Income Tax?

New York income tax is characterized by its progressive structure, meaning the tax rate increases as income rises. This system is designed to ensure that individuals with higher earnings contribute a larger share of their income to support public services and infrastructure. For example, someone earning $50,000 annually will pay a lower percentage of their income in taxes compared to someone earning $500,000. The progressive nature of the tax system aims to create a balanced approach to taxation, where wealthier individuals contribute more to the state's revenue.

Another key feature of New York income tax is the presence of both state and local taxes. Residents of New York City, for instance, must pay an additional city income tax on top of their state tax. This dual taxation system can increase the overall tax burden for urban residents. However, the state offers various deductions and credits to offset these additional costs. For example, taxpayers can claim deductions for mortgage interest, charitable contributions, and certain business expenses. These deductions help reduce the taxable income, thereby lowering the overall tax liability.

In addition to deductions, New York provides several tax credits to assist specific groups, such as low-income families, seniors, and disabled individuals. These credits are designed to alleviate the financial burden on vulnerable populations. For instance, the Earned Income Tax Credit (EITC) provides a refundable credit to working families with low to moderate incomes. Similarly, the Senior Citizens Exemption Program offers property tax relief to eligible senior citizens, reducing their overall tax obligations. Understanding these features is essential for maximizing your tax benefits and minimizing your liabilities.

How Does New York Income Tax Affect Different Income Brackets?

The impact of New York income tax varies significantly across different income brackets. For low-income earners, the tax burden is relatively light due to the progressive nature of the tax system. Individuals earning below the standard deduction threshold may not owe any state income tax at all. For example, a single filer earning $20,000 annually might only pay a few hundred dollars in state taxes, depending on their deductions and credits. This low tax liability helps ensure that low-income individuals can meet their basic needs without excessive financial strain.

Middle-income earners, on the other hand, face a moderate tax burden. As their income increases, so does their tax rate. For example, a family of four earning $100,000 annually might fall into the middle tax bracket, paying around 6% of their income in state taxes. However, they can take advantage of various deductions and credits to reduce their taxable income. For instance, they might claim the child tax credit, mortgage interest deduction, or education credit to lower their overall tax liability. These strategies can significantly impact their net income, making it easier to manage household expenses.

High-income earners experience the highest tax burden due to the progressive tax structure. For example, an individual earning $500,000 annually might fall into the top tax bracket, paying upwards of 10% of their income in state taxes. While they have access to the same deductions and credits as lower-income taxpayers, the sheer volume of their earnings results in a larger tax bill. To mitigate this, high-income earners often consult with tax professionals to explore advanced tax planning strategies, such as establishing retirement accounts or investing in tax-efficient vehicles.

Read also:Exploring The World Of Movierulz 2025 Kannada A Comprehensive Guide

Why Is New York Income Tax Important for Residents?

New York income tax plays a vital role in funding essential services and infrastructure across the state. The revenue generated from income taxes supports public schools, healthcare facilities, transportation systems, and emergency services. Without this funding, the state would struggle to maintain its high standard of living and quality of life. For example, income tax dollars help pay for teacher salaries, road maintenance, and public safety initiatives, ensuring that residents have access to safe and well-maintained communities.

Furthermore, New York income tax contributes to the state's economic stability and growth. By collecting taxes from residents, the state can invest in programs that stimulate job creation and business development. For instance, tax revenue may be used to fund small business grants, workforce training programs, or infrastructure projects that attract new industries to the state. These investments not only benefit taxpayers but also enhance the overall economic vitality of New York.

Finally, paying New York income tax is a civic responsibility that fosters a sense of community and shared purpose. When residents contribute to the state's revenue, they are investing in the well-being of their neighbors and the future of their communities. This collective effort ensures that everyone has access to the resources and services needed to thrive. By understanding and fulfilling their tax obligations, New Yorkers can take pride in their role in shaping the state's future.

How Can You Reduce Your New York Income Tax Liability?

Reducing your New York income tax liability involves taking advantage of available deductions, credits, and exemptions. One of the most effective strategies is to maximize your itemized deductions. This includes expenses such as mortgage interest, property taxes, medical expenses, and charitable contributions. By itemizing these deductions, you can significantly lower your taxable income, resulting in a reduced tax bill. For example, if you paid $10,000 in mortgage interest and $5,000 in property taxes, you could deduct these amounts from your gross income, lowering your taxable income by $15,000.

Another way to reduce your tax liability is to claim eligible tax credits. New York offers a variety of credits, including the Child and Dependent Care Credit, the Education Credit, and the Earned Income Tax Credit (EITC). These credits provide direct reductions in your tax obligation, dollar for dollar. For instance, if you qualify for a $1,000 education credit, your tax bill will be reduced by that amount. Additionally, some credits are refundable, meaning you can receive a refund even if your credit exceeds your tax liability.

Finally, consider contributing to tax-advantaged accounts, such as retirement plans or health savings accounts (HSAs). Contributions to these accounts are typically made with pre-tax dollars, reducing your taxable income for the year. For example, if you contribute $5,000 to your 401(k), your taxable income will decrease by that amount. This strategy not only lowers your current tax liability but also helps you save for future expenses, such as retirement or medical costs.

What Are the Common Mistakes to Avoid When Filing New York Income Tax?

One common mistake taxpayers make when filing New York income tax is failing to claim all eligible deductions and credits. Many individuals overlook valuable tax breaks, such as the Earned Income Tax Credit (EITC) or the Child Tax Credit, resulting in higher tax bills. To avoid this mistake, carefully review your tax forms and consult with a tax professional if necessary. They can help identify any deductions or credits you may have missed and ensure you receive the maximum benefit.

Another frequent error is miscalculating your taxable income. This can happen if you fail to account for all sources of income, such as freelance work, rental income, or investment gains. To prevent this mistake, keep detailed records of all your income sources throughout the year. Use tools like spreadsheets or tax software to organize your financial information and ensure accuracy when calculating your taxable income.

Frequently Asked Questions About New York Income Tax

1. Do I Need to File New York Income Tax If I Live Out of State but Work in New York?

Yes, if you live out of state but work in New York, you are generally required to file a New York state income tax return. New York has reciprocal agreements with some neighboring states, such as New Jersey and Pennsylvania, which may exempt you from filing in both states. However, if you live in a state without such an agreement, you will need to file a nonresident New York tax return to report your New York-source income.

2. Can I Deduct State and Local Taxes on My Federal Return?

Yes, under the Tax Cuts and Jobs Act (TCJA), you can deduct state and local taxes (SALT) on your federal return, up to a cap of $10,000. This deduction includes property taxes and either state income taxes or sales taxes, but not both. Be sure to consult with a tax professional to determine the best strategy for maximizing your SALT deduction while minimizing your overall tax liability.

Is New York Income Tax Fair for All Taxpayers?

The fairness of New York income tax is a topic of ongoing debate among policymakers, economists, and taxpayers. Proponents of the current system argue that its progressive structure ensures that wealthier individuals contribute a larger share of their income, reflecting their greater ability to pay. This approach helps fund essential services and infrastructure, benefiting all residents regardless of income level. For example, public schools, healthcare facilities, and transportation systems are accessible to everyone, regardless of their tax bracket.

However, critics contend that the tax system places an undue burden on high-income earners, potentially discouraging investment and job creation. They argue that a flatter tax rate would promote economic growth by incentivizing entrepreneurship and innovation. Additionally, some believe that the dual taxation system in New York City creates an unfair disadvantage for urban residents, who must pay both state and city income taxes.

Ultimately, the fairness of New York income tax depends on individual perspectives and priorities. While some view the progressive system as equitable and just, others see it as overly burdensome. As the state continues to evolve, policymakers will need to balance competing interests to create a tax system that meets the needs of all residents.

How Do New York Income Tax Rates Compare to Other States?

New York income tax rates are relatively high compared to other states, particularly those with no income tax, such as Texas and Florida. However, when compared to states with similar economic profiles, such as California and Illinois, New York's rates are comparable. For example, California's top tax rate is 13.3%, slightly higher than New York's 10.9%. Illinois, on the other hand, has a flat tax rate of 4.95%, making it more favorable for high-income earners.

It's important to note that tax rates are just one factor to consider when evaluating the overall tax burden. Other factors, such as property taxes, sales taxes, and local taxes, can significantly impact a resident's total tax liability. For instance, while New York's income tax rates may be higher than some states, its property tax rates are relatively moderate. This balance helps ensure that residents are not overburdened by any single tax category.

In conclusion, New York income tax rates are competitive with other states of similar size and economic complexity. While they may be higher than some states, they are offset by a range of deductions, credits, and exemptions that help reduce the overall tax burden. By understanding these factors, residents can make informed decisions about their finances and take advantage of available tax benefits.

Conclusion

New York income tax is a complex but essential aspect of financial planning for residents across the state. By understanding the key features, impacts, and strategies for reducing your tax liability, you can make informed decisions about your finances and ensure compliance with state regulations. Whether you're a low-income earner, middle-class family, or high-net-worth individual, the state offers a range of tools and resources to help you navigate the tax landscape. Remember to stay informed about legislative updates and consult with a tax professional if needed. With the right knowledge and preparation, you