New York income tax is a critical aspect of financial planning for residents of the Empire State. Whether you're a recent transplant or a lifelong New Yorker, understanding how the state's income tax system works is essential for optimizing your finances and avoiding potential penalties. With one of the highest state income tax rates in the country, New York requires careful attention to detail when it comes to filing taxes. This article aims to demystify the complexities of New York income tax by providing a detailed overview of its structure, key considerations, and practical tips for staying compliant.

Residents of New York State are subject to both federal and state income taxes, with the latter being governed by specific laws and regulations. The state employs a progressive tax system, meaning that higher income levels are taxed at progressively higher rates. Additionally, New York City imposes its own income tax on residents, adding another layer of complexity for those living within city limits. Understanding these nuances is crucial for ensuring accurate tax filings and maximizing deductions and credits.

As we delve deeper into this topic, you'll discover how New York income tax impacts various aspects of your financial life. From determining your taxable income to navigating deductions and credits, this guide will provide you with the knowledge and tools necessary to manage your tax obligations effectively. Whether you're a seasoned taxpayer or new to the process, the insights shared here will empower you to make informed decisions and potentially reduce your tax liability.

Read also:Will Arnett Alessandra Brawn Split A Comprehensive Look Into Their Relationship Journey

What Is New York Income Tax?

New York income tax refers to the state's system of taxing the earnings of individuals, businesses, and other entities residing or operating within its borders. Administered by the New York State Department of Taxation and Finance, this tax is levied on various forms of income, including wages, salaries, tips, investment earnings, and business profits. The primary purpose of New York income tax is to generate revenue for the state government, which funds essential services such as education, healthcare, infrastructure, and public safety.

The tax structure in New York is progressive, meaning that different income brackets are taxed at varying rates. For instance, lower-income individuals pay a smaller percentage of their earnings in taxes compared to higher-income earners. This approach aims to ensure that the tax burden is distributed more equitably across the population. Additionally, New York offers a range of deductions and credits designed to alleviate the financial strain on certain groups, such as low-income families, seniors, and disabled individuals.

It's worth noting that New York City residents face an additional layer of taxation in the form of city income tax. This local tax is calculated separately from the state tax and is based on a resident's income level. Together, these taxes contribute significantly to the overall tax burden for individuals living in the city. Understanding the interplay between state and local taxes is essential for residents seeking to minimize their tax liabilities.

How Does New York Income Tax Compare to Other States?

When evaluating New York income tax, it's helpful to compare it to the tax systems of other states. Among the 50 states, New York ranks among the highest in terms of income tax rates. For example, while some states like Florida and Texas impose no state income tax, New York's top marginal rate exceeds 10% for high-income earners. This disparity can have a substantial impact on individuals considering a move to or from the state.

Furthermore, New York's tax system includes unique features that set it apart from other states. For instance, the state offers a variety of tax incentives for businesses and individuals, such as the New York State Homeowners' Tax Credit and the Empire State Film Production Tax Credit. These programs aim to stimulate economic growth and attract investment to the state. However, navigating these incentives can be complex, requiring careful planning and expert guidance.

In addition to its relatively high tax rates, New York also imposes strict filing deadlines and penalties for non-compliance. Residents who fail to file their taxes on time or underreport their income may face significant fines and interest charges. This underscores the importance of staying informed about New York's tax laws and seeking professional advice when necessary.

Read also:The Ultimate Guide To Exploring Kannada 5movierulz 2025 A Deep Dive Into The World Of Entertainment

What Are the Key Features of New York Income Tax?

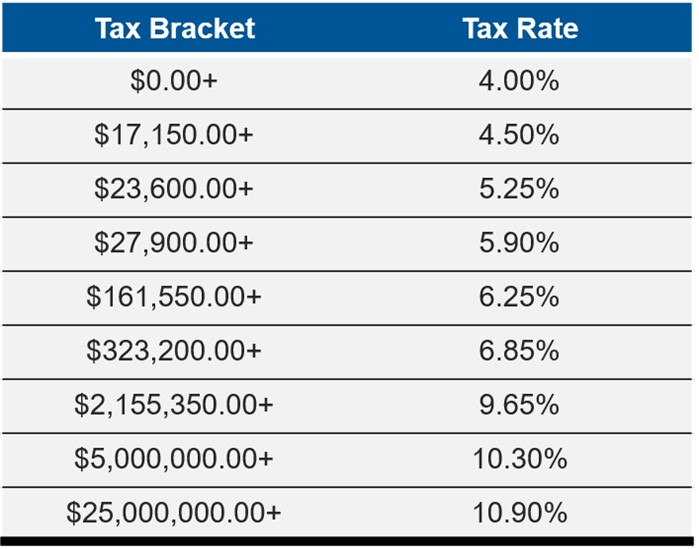

Several key features distinguish New York income tax from other states' systems. First and foremost, the state employs a progressive tax structure, with rates increasing as income levels rise. For the 2023 tax year, the lowest marginal rate is 4%, while the highest rate reaches 10.9% for single filers earning over $2.5 million annually. These rates are subject to change, so it's important for taxpayers to stay updated on any legislative developments.

Another notable feature of New York income tax is the availability of numerous deductions and credits. These include the New York State Earned Income Tax Credit, the Child and Dependent Care Credit, and the Homeowners' Tax Credit, among others. By claiming these deductions and credits, taxpayers can potentially reduce their overall tax liability and retain more of their earnings. However, eligibility requirements and calculation methods vary for each benefit, necessitating thorough research or consultation with a tax professional.

Finally, New York's tax system is closely integrated with federal tax laws, requiring residents to consider both state and federal implications when preparing their returns. This synchronization can simplify the filing process but also demands a comprehensive understanding of both jurisdictions' regulations. For instance, certain deductions allowed at the federal level may not be applicable at the state level, and vice versa.

Who Is Subject to New York Income Tax?

Not all individuals residing in New York are subject to the state's income tax. Generally, the tax applies to residents, part-year residents, and nonresidents who earn income from New York sources. Full-time residents are taxed on their worldwide income, regardless of where it is earned. Part-year residents, on the other hand, are taxed only on the income they earn while living in New York. Nonresidents are taxed solely on income derived from New York-based activities, such as employment or investments in the state.

It's important to note that determining residency status can be complex and may involve evaluating factors such as the length of time spent in the state, the location of primary residence, and the nature of income earned. The New York State Department of Taxation and Finance provides specific guidelines for establishing residency, which taxpayers should carefully review to ensure accurate classification. Misclassifying one's residency status can lead to overpayment or underpayment of taxes, resulting in penalties or audits.

In addition to individual taxpayers, businesses operating in New York are also subject to income tax. This includes corporations, partnerships, sole proprietorships, and other entities earning income within the state. Business income is typically reported separately from personal income, with its own set of rules and regulations governing taxation. Understanding these distinctions is crucial for business owners seeking to comply with New York's tax laws and optimize their financial strategies.

How Do You Determine Residency Status for Tax Purposes?

Determining residency status for New York income tax purposes involves evaluating several criteria established by the state. The primary test considers whether an individual maintains a permanent place of abode in New York and spends more than 183 days within the state during the tax year. If both conditions are met, the individual is classified as a resident for tax purposes. However, exceptions exist for individuals who can demonstrate that their primary residence is located outside of New York.

For part-year residents, the determination process focuses on identifying the portion of the year spent in New York and the corresponding income earned during that period. This requires meticulous record-keeping and may involve consulting with a tax advisor to ensure accurate calculations. Nonresidents, meanwhile, must carefully track their New York-source income and report it separately from their income earned in other jurisdictions.

Given the potential complexity of residency determinations, taxpayers often benefit from seeking professional guidance. Tax advisors familiar with New York's regulations can help clarify ambiguities and ensure compliance with applicable laws. Additionally, staying informed about any changes to residency criteria or filing requirements can prevent costly mistakes and simplify the tax filing process.

Can You Be a Resident of Two States Simultaneously?

While it's possible to maintain residences in multiple states, being classified as a resident of two states simultaneously for tax purposes is rare. Most states, including New York, adhere to the principle of "domicile," which refers to an individual's permanent legal residence. Under this framework, individuals are generally considered residents of only one state at a time, even if they own property or spend significant time in another state.

However, complications can arise when individuals divide their time between two states or maintain significant connections to both. In such cases, determining residency status may require evaluating factors such as the location of primary residence, voting registration, driver's license issuance, and the state where dependents reside. Taxpayers facing these situations should consult with a tax professional to navigate the complexities and ensure proper classification.

How Is New York Income Tax Calculated?

Calculating New York income tax involves several steps, beginning with determining your taxable income. Taxable income is calculated by subtracting allowable deductions and exemptions from your gross income. Gross income includes wages, salaries, tips, investment earnings, and other forms of compensation. Once taxable income is established, it is applied to the appropriate tax brackets to determine the amount of tax owed.

New York's tax brackets are structured progressively, with higher income levels subject to higher tax rates. For example, in 2023, single filers earning up to $8,500 are taxed at a rate of 4%, while those earning between $215,400 and $1,077,550 are taxed at 8.82%. These rates are subject to change annually, so it's important to refer to the most recent tax tables when calculating your liability. Additionally, certain deductions and credits may further reduce the amount of tax owed, making it essential to account for these factors during the calculation process.

For New York City residents, the calculation process becomes more intricate due to the addition of city income tax. This local tax is calculated separately from the state tax and is based on a resident's income level. The combined effect of state and city taxes can significantly increase the overall tax burden for individuals living in the city, underscoring the importance of careful planning and accurate calculations.

What Are the Most Common Deductions and Credits?

New York offers a variety of deductions and credits designed to reduce the tax burden on eligible taxpayers. Among the most common are the New York State Earned Income Tax Credit, the Child and Dependent Care Credit, and the Homeowners' Tax Credit. The Earned Income Tax Credit provides financial relief to low- and moderate-income working individuals and families, with the credit amount varying based on income level and family size.

The Child and Dependent Care Credit helps offset the costs of childcare and dependent care expenses incurred while working or looking for work. Eligible taxpayers can claim up to 35% of their qualifying expenses, subject to certain income limitations. Similarly, the Homeowners' Tax Credit aims to reduce property taxes for eligible homeowners, with the credit amount determined by factors such as income, property value, and location.

Other notable credits include the New York State Child Tax Credit, the Disabled Persons Credit, and the Senior Citizens' Real Property Tax Credit. Each of these credits has specific eligibility requirements and calculation methods, necessitating careful consideration during the tax preparation process. By leveraging these deductions and credits, taxpayers can potentially reduce their overall tax liability and retain more of their hard-earned income.

Why Is It Important to Maximize Deductions and Credits?

Maximizing deductions and credits is crucial for minimizing New York income tax liability and optimizing financial well-being. By reducing taxable income through allowable deductions and claiming eligible credits, taxpayers can lower the amount of tax owed and increase their take-home pay. This is particularly important for individuals and families facing financial challenges or seeking to build savings.

In addition to immediate financial benefits, maximizing deductions and credits can also contribute to long-term financial stability. For example, reducing taxable income through retirement account contributions not only lowers current tax liability but also helps build a nest egg for future needs. Similarly, claiming education-related credits can ease the burden of student loan repayments and promote continued learning and career advancement.

What Are the Penalties for Non-Compliance?

Failing to comply with New York income tax regulations can result in significant penalties and interest charges. These penalties are designed to discourage non-compliance and ensure that all residents contribute their fair share to state revenue. For instance, individuals who file their taxes late may be subject to a penalty equal to 5% of the unpaid tax for each month or part of a month the return is late, up to a maximum of 25%. Additionally, interest is charged on the unpaid tax at a rate determined by the state.

Underreporting income or claiming ineligible deductions and credits can lead to further penalties, including fines and potential audits. The New York State Department of Taxation and Finance employs sophisticated systems for detecting discrepancies and ensuring compliance, making it imperative for taxpayers to maintain accurate records and adhere to all applicable laws. In severe cases, non-compliance may result in legal action or criminal prosecution, underscoring the importance of timely and accurate tax filings.

To avoid penalties, taxpayers should familiarize themselves with New York's tax laws and seek professional guidance when necessary. Keeping thorough records, understanding eligibility requirements for deductions and credits, and filing returns by the established deadlines are all essential steps for ensuring compliance and avoiding unnecessary financial burdens.

How Can You Avoid Common Mistakes When Filing?

Avoiding common mistakes when filing New York income tax returns is essential for ensuring accuracy and minimizing the risk of penalties. One of the most frequent errors is failing to report all sources of income, including side jobs, freelance work, and investment earnings. Taxpayers should carefully review all W-2s, 10