Residents of New York State face one of the most complex tax systems in the United States, making it crucial to understand NY income tax thoroughly. As of 2023, New York has a progressive tax system that adjusts based on income levels, impacting individuals and businesses alike. With numerous deductions, credits, and exemptions available, navigating NY income tax can be overwhelming without proper guidance. Whether you're a newly employed resident or a seasoned taxpayer, staying informed about changes and updates is essential for maximizing your financial health.

NY income tax isn't just about filing forms annually; it's about understanding how the state calculates your liability and what strategies can help reduce your burden. From standard deductions to itemized ones, taxpayers have options tailored to their financial situations. Moreover, New York State offers specific credits for families, senior citizens, and those with disabilities, ensuring fairness in taxation. Keeping abreast of these provisions ensures compliance while optimizing refunds.

As we delve deeper into this topic, we'll explore key aspects of NY income tax, including rates, deadlines, exemptions, and strategies for minimizing liabilities. This guide aims to provide clarity on often-confusing tax codes, empowering taxpayers to make informed decisions. Whether you're filing individually or managing a business entity, having a solid grasp of NY income tax principles will benefit both your personal finances and professional endeavors.

Read also:Unveiling The Allure Of Lara Rose Erome A Rising Star In The Spotlight

Table of Contents

- What Are the Current NY Income Tax Rates?

- Exploring Deductions and Exemptions in NY Income Tax

- How to File Your NY Income Tax Return

- Understanding Tax Credits Available for NY Residents

- When Are NY Income Tax Deadlines?

- What Happens If You Miss NY Income Tax Deadlines?

- How Does NY Income Tax Affect Businesses?

- Is NY Income Tax Different for Retirees?

- Frequently Asked Questions About NY Income Tax

What Are the Current NY Income Tax Rates?

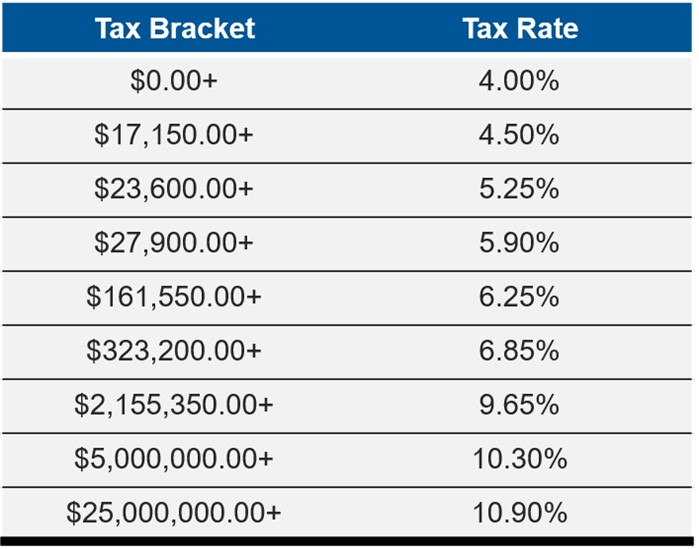

NY income tax rates are structured progressively, meaning higher earners pay a larger percentage of their income compared to lower-income individuals. For the tax year 2023, New York State imposes seven brackets ranging from 4% to 10.9% depending on taxable income. Single filers earning up to $8,600 fall under the lowest bracket at 4%, whereas those earning over $25 million are taxed at the highest rate of 10.9%. Joint filers enjoy slightly higher thresholds but follow the same percentage scale.

This structure aims to balance revenue generation with taxpayer fairness. The state regularly reviews and adjusts these rates to account for inflation and economic changes. Additionally, localities within New York may impose supplemental taxes, further complicating calculations. Understanding where your income falls within these brackets is vital for accurate tax planning.

For instance, if you're a single filer earning $50,000 annually, your effective tax rate would likely hover around 6.45%, assuming no additional deductions or credits apply. It's important to note that while the marginal rate increases with income, only the portion exceeding each bracket's threshold gets taxed at the higher rate. This ensures a gradual increase rather than an abrupt jump in liability.

Exploring Deductions and Exemptions in NY Income Tax

Deductions play a critical role in reducing taxable income, thereby lowering NY income tax liabilities. Taxpayers can choose between standard or itemized deductions, depending on which offers greater benefits. For 2023, single filers receive a standard deduction of $8,950, while married couples filing jointly get $17,900. These amounts increase annually based on cost-of-living adjustments.

Itemizing deductions allows taxpayers to claim specific expenses like mortgage interest, charitable contributions, and medical bills exceeding 7.5% of adjusted gross income (AGI). However, this method requires thorough record-keeping and often involves professional assistance. Exemptions further reduce taxable income by providing credits for dependents, seniors, and individuals with disabilities.

Let's consider an example: A married couple with two children earning $100,000 annually might qualify for personal exemptions totaling $16,000 ($4,000 per person). If they also itemize deductions totaling $20,000, their taxable income drops significantly, resulting in lower NY income tax obligations. Carefully evaluating these options ensures optimal savings.

Read also:Red Half Up Half Down The Ultimate Guide To A Bold And Trendy Hairstyle

How to File Your NY Income Tax Return

Filing NY income tax returns involves several steps, starting with gathering necessary documents such as W-2s, 1099s, and receipts for deductible expenses. Residents can file electronically through the New York State Department of Taxation and Finance website or via certified tax preparation software. Electronic filing expedites processing times and reduces errors, making it the preferred method for most taxpayers.

Alternatively, paper forms remain available for those who prefer traditional methods. Form IT-201 is used by individuals, while businesses utilize various specialized forms based on entity type. Regardless of method chosen, ensuring accuracy and completeness prevents delays or penalties. Including all required schedules and attachments supports claims made within the return.

Here’s a quick checklist to follow when preparing to file:

- Gather all income statements and expense receipts.

- Choose between standard or itemized deductions.

- Review eligibility for available credits and exemptions.

- Double-check calculations before submission.

Understanding Tax Credits Available for NY Residents

Tax credits differ from deductions in that they directly reduce the amount of tax owed rather than simply lowering taxable income. NY residents benefit from numerous credits designed to assist specific groups or promote certain behaviors. Examples include the Earned Income Tax Credit (EITC) for low-to-moderate-income workers, Child Care Credit for working parents, and Homeowners' Credit for property owners.

Additionally, New York offers unique credits not found in other states. The Excelsior Jobs Program provides incentives for businesses creating jobs within the state, while the Mortgage Credit Certificate Program assists first-time homebuyers. Applying for these credits requires meeting specific criteria and completing additional forms during the filing process.

It's worth noting that some credits are refundable, meaning taxpayers receive a refund even if the credit exceeds their total tax liability. Others are non-refundable, limiting benefits to the extent of taxes owed. Consulting with a tax professional helps identify applicable credits and ensures proper application.

When Are NY Income Tax Deadlines?

NY income tax deadlines align closely with federal deadlines, typically falling on April 15th each year unless the date lands on a weekend or holiday. In such cases, the deadline shifts to the next business day. Extensions are available upon request, granting an additional six months to file without penalty. However, any taxes owed must still be paid by the original deadline to avoid interest and late payment fees.

Businesses face different deadlines depending on entity type and fiscal year-end. Partnerships and S corporations generally file by March 15th, while C corporations have until April 15th. Keeping track of these varying dates prevents unnecessary complications. Setting reminders or working with accountants ensures timely submissions.

For example, a small business owner operating as an LLC might file their personal return by April 15th but submit partnership information by March 15th. Coordinating these tasks requires careful planning and organization. Missing deadlines, even with extensions, can lead to severe consequences including fines and increased interest rates.

What Happens If You Miss NY Income Tax Deadlines?

Missing NY income tax deadlines triggers automatic penalties and interest charges on unpaid balances. Failure-to-file penalties start at 5% of unpaid taxes per month, up to a maximum of 25%. Failure-to-pay penalties accrue at 0.5% monthly, compounding until paid in full. Interest rates vary annually but generally hover around 3-5%, compounding daily.

These penalties quickly add up, potentially doubling the original tax owed if left unaddressed. Taxpayers facing difficulties meeting deadlines should communicate with the Department of Taxation and Finance to explore payment plans or abatement options. Demonstrating good faith efforts often leads to reduced penalties or extended payment terms.

Consider a scenario where a taxpayer owes $5,000 in NY income tax but misses the deadline by three months. They could face $750 in failure-to-file penalties ($5,000 x 5% x 3 months), $75 in failure-to-pay penalties ($5,000 x 0.5% x 3 months), and approximately $375 in interest charges, totaling nearly $1,200 in additional costs. Avoiding such outcomes underscores the importance of timely filings.

How Does NY Income Tax Affect Businesses?

NY income tax regulations extend beyond individual taxpayers, impacting businesses operating within the state. Corporations, partnerships, and sole proprietorships all face unique requirements based on structure and activities. Corporate entities pay a flat rate of 6.5% on net income, plus an additional Metropolitan Commuter Transportation District surcharge of 0.34% for those located in specific counties.

Partnerships and LLCs pass through profits to individual members, who then report their share on personal returns. However, these entities still file informational returns using Form IT-203. Sole proprietors include business income directly on their Form IT-201, treating it as personal income. Special rules apply to out-of-state businesses generating revenue within New York, requiring nexus determinations and potential filings.

Managing business taxes involves tracking expenses, maintaining accurate records, and adhering to deadlines. Utilizing accounting software or hiring professionals simplifies compliance and optimizes deductions. Staying informed about legislative changes ensures ongoing adherence to evolving regulations.

Is NY Income Tax Different for Retirees?

Retirees receive special consideration under NY income tax laws, with several provisions designed to ease financial burdens. Social Security benefits remain exempt from taxation regardless of income level, unlike federal rules. Additionally, pensions and retirement account distributions qualify for a $20,000 exemption for those aged 59½ or older. These benefits help preserve savings during retirement years.

However, retirees must still report other sources of income, including interest, dividends, and rental properties. Deductions and credits available to working individuals generally apply equally to retirees, providing further opportunities for reduction. Consulting with financial advisors specializing in retirement planning ensures comprehensive strategies addressing both current and future needs.

For instance, a retiree drawing $30,000 annually from Social Security and $25,000 from a pension would exclude the entire Social Security amount and $20,000 of pension income, leaving only $5,000 subject to NY income tax. Leveraging available exemptions significantly lowers overall liabilities, enhancing quality of life during retirement.

Frequently Asked Questions About NY Income Tax

Q1: Can I Deduct State Taxes on My Federal Return?

Yes, under the SALT (State and Local Tax) deduction cap, taxpayers can deduct up to $10,000 in combined state income, sales, and property taxes on their federal returns. This limit applies regardless of filing status or number of dependents. Proper documentation ensures accurate claims and maximizes allowable deductions.

Q2: What Happens If I Move Out of State Mid-Year?

Moving out of New York mid-year requires prorating income based on residency periods. Former residents file Form IT-203-NR, reporting only income earned while living in the state. New York considers anyone maintaining a permanent residence within its borders a resident unless proven otherwise. Consulting a tax professional clarifies complex situations involving dual-state liabilities.

Q3: Are There Any Special Provisions for Military Personnel?

Military personnel stationed in New York but maintaining another state as their legal residence may avoid NY income tax obligations. Service members must provide proof of domicile to qualify for exemptions. Additionally, combat pay remains exempt from both federal and state taxation, offering significant savings opportunities.

Conclusion

Navigating NY income tax requires understanding its complexities and leveraging available resources to optimize outcomes. From progressive rates and numerous deductions to specialized credits and unique provisions for specific groups, staying informed empowers taxpayers to make smart financial decisions. Whether you're an individual filer or business owner, adhering to deadlines, maintaining accurate records, and seeking professional guidance when needed ensures compliance and minimizes liabilities.

As always, remaining vigilant about legislative changes and regulatory updates helps maintain readiness for upcoming filing seasons. Embracing technology through electronic filing and accounting software streamlines processes, reducing stress and increasing accuracy. Remember, proactive planning and thorough preparation pave the way for successful tax management and improved financial stability.