New York State income tax plays a pivotal role in shaping the financial landscape for residents across the Empire State. As one of the largest revenue sources for the state government, this tax system directly impacts individuals, families, and businesses alike. Whether you're a long-time resident or a newcomer, understanding how New York State income tax works is essential for effective financial planning and compliance. From progressive tax brackets to deductions and credits, navigating this intricate system can seem overwhelming. However, armed with the right knowledge, you can confidently manage your obligations while maximizing potential savings.

Residents often find themselves asking key questions about their tax responsibilities: How much will I owe? What deductions am I eligible for? Can I claim specific credits? The answers lie within the complex framework of New York State income tax laws. These laws are designed to ensure equitable contributions from all income levels while offering relief to those who need it most. By staying informed about recent changes, deadlines, and available resources, taxpayers can better prepare for each filing season.

Moreover, as New York continues to refine its tax policies, staying updated becomes even more critical. Recent legislative updates may affect everything from standard deductions to itemized expenses. For example, changes in federal tax laws can have ripple effects on state filings, making it crucial to consult both state and federal guidelines when preparing your return. This article aims to demystify the process by providing actionable insights, practical tips, and expert advice tailored specifically for New York taxpayers.

Read also:How Safe Is Ullu Webseries Download Movierulz In 2023

Table of Contents

- 1. What Is New York State Income Tax?

- 2. Who Must File New York State Income Tax?

- 3. How Are Tax Brackets Determined in New York?

- 4. Can You Claim Deductions on New York State Income Tax?

- 5. Exploring Credits Available for New York Taxpayers

- 6. How Does New York State Income Tax Compare to Other States?

- 7. Common Mistakes to Avoid When Filing Your Taxes

- 8. Frequently Asked Questions About New York State Income Tax

What Is New York State Income Tax?

New York State income tax refers to the mandatory tax levied on the earnings of individuals, corporations, and other entities residing or operating within the state. Administered by the New York State Department of Taxation and Finance, this tax contributes significantly to funding essential public services such as education, healthcare, infrastructure, and public safety. Understanding its purpose and structure is the first step toward effective compliance.

The tax system in New York operates on a progressive scale, meaning that higher-income earners are taxed at a greater percentage than those with lower incomes. This approach aims to create a fair distribution of financial responsibility across different economic strata. Additionally, the state offers various deductions and credits to help alleviate the tax burden for eligible taxpayers.

For instance, individuals may qualify for deductions related to mortgage interest, charitable contributions, and student loan repayments. Similarly, credits such as the Earned Income Tax Credit (EITC) and Child Care Credit provide targeted relief to specific groups. By familiarizing yourself with these provisions, you can take full advantage of opportunities to reduce your taxable income.

Who Must File New York State Income Tax?

Not everyone residing in New York is required to file a state income tax return. The obligation depends on several factors, including your filing status, income level, and whether you meet certain thresholds. Generally, if your gross income exceeds the minimum limits set by the state, you must submit a return. These limits vary based on your filing status—single, married filing jointly, head of household, etc.

Non-residents who earn income from sources within New York State may also be subject to taxation. This includes individuals working remotely for New York-based employers or engaging in business activities within the state. Part-year residents, those who move into or out of New York during the tax year, must apportion their income accordingly when filing their returns.

It’s important to note that failing to file when required can result in penalties and interest charges. To avoid complications, consult the latest guidelines provided by the New York State Department of Taxation and Finance or seek advice from a qualified tax professional.

Read also:Anthony Merseal The Rising Star You Need To Know About

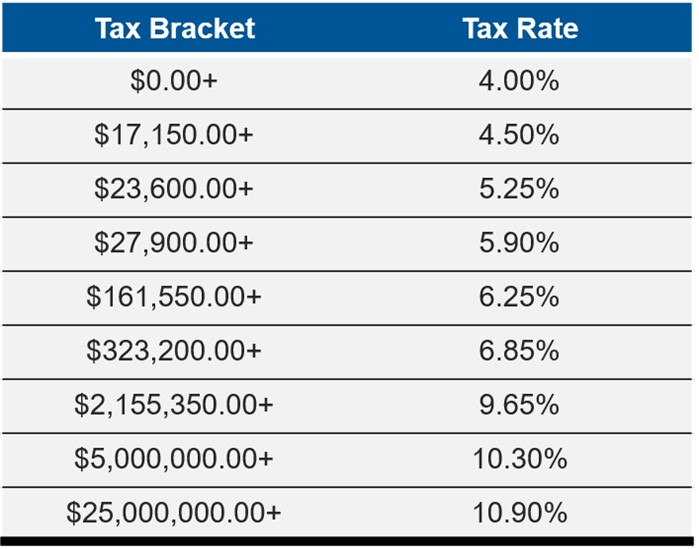

How Are Tax Brackets Determined in New York?

Tax brackets in New York State determine the rate at which your income is taxed. These brackets are structured progressively, with higher rates applying to portions of income above specified thresholds. For example, as of the most recent tax year, the lowest bracket applies to taxable income up to a certain amount, while the highest bracket affects income exceeding another threshold.

Here’s a breakdown of the current tax brackets for single filers:

- Up to $8,500: 4%

- $8,501–$11,700: 4.5%

- $11,701–$13,900: 5.25%

- $13,901–$21,800: 5.9%

- $21,801–$80,650: 6.33%

- $80,651–$215,400: 6.65%

- $215,401–$1,077,550: 6.85%

- Above $1,077,550: 8.82%

These brackets are adjusted annually to account for inflation and other economic factors. It’s worth noting that additional surcharges may apply for high-income earners in certain metropolitan areas, such as New York City.

Can You Claim Deductions on New York State Income Tax?

Yes, New York State allows taxpayers to claim various deductions to reduce their taxable income. These deductions fall into two primary categories: standard and itemized. Choosing between them depends on your individual circumstances and which option yields the greatest benefit.

The standard deduction provides a fixed amount that reduces your taxable income without requiring detailed records. For 2023, the standard deduction for single filers is $8,400, while married couples filing jointly can claim $16,800. However, if your total itemized deductions exceed these amounts, opting for itemization could result in greater savings.

Itemized deductions cover a broader range of expenses, including but not limited to:

- Mortgage interest

- Property taxes

- Medical and dental expenses exceeding 7.5% of adjusted gross income (AGI)

- Charitable contributions

- Casualty or theft losses

Be sure to retain thorough documentation for any itemized deductions you claim, as the IRS and New York State may request verification during audits or reviews.

Are There Limits on Itemized Deductions?

Indeed, there are limitations on certain itemized deductions under both federal and New York State tax laws. For example, the SALT (State and Local Tax) deduction cap remains at $10,000 per year for federal purposes. While New York does not impose an additional cap, taxpayers should carefully calculate their deductions to ensure compliance with all applicable rules.

Additionally, some deductions phase out for higher-income earners. Known as Pease limitations, these reductions apply to itemized deductions for taxpayers with AGI above specified thresholds. Consulting a tax advisor can help you navigate these complexities and optimize your deductions.

Exploring Credits Available for New York Taxpayers

Credits offer another valuable way to lower your New York State income tax liability. Unlike deductions, which reduce taxable income, credits directly decrease the amount of tax owed, making them particularly beneficial. Several credits are available to eligible taxpayers, addressing diverse needs such as family support, education expenses, and energy efficiency.

One of the most widely used credits is the Earned Income Tax Credit (EITC), designed to assist low- to moderate-income working individuals and families. Qualifying factors include earned income, filing status, and dependent status. Another popular credit is the Child Care Credit, which helps offset the cost of childcare services for working parents.

Energy-conscious homeowners may benefit from the Residential Energy Credit, which incentivizes investments in renewable energy systems like solar panels. Similarly, the Property Tax Credit provides relief to homeowners facing escalating property tax bills.

How Do I Know If I Qualify for a Credit?

Eligibility criteria vary depending on the specific credit. To determine whether you qualify, review the official guidelines provided by the New York State Department of Taxation and Finance. Many credits also require submission of supporting documentation, so maintaining accurate records is crucial.

For example, claiming the EITC typically involves providing proof of earned income, social security numbers for yourself and dependents, and evidence of residency in New York State for more than half the year. Tools like the EITC Assistant on the IRS website can help streamline the qualification process.

How Does New York State Income Tax Compare to Other States?

When evaluating New York State income tax, it’s helpful to compare it to other states’ systems. While some states impose flat-rate taxes or no income tax at all, New York’s progressive structure ensures that higher-income earners contribute proportionally more. This approach aligns with the state’s commitment to funding vital public services.

In contrast, neighboring states like Pennsylvania and New Jersey use different methodologies. Pennsylvania levies a flat rate of 3.07% on all taxpayers, regardless of income level. Meanwhile, New Jersey employs a hybrid system combining progressive rates with additional surcharges for top earners. Each state’s approach reflects its unique fiscal priorities and economic conditions.

For individuals considering relocation or remote work arrangements, understanding these differences can inform decision-making. Tools like cost-of-living calculators and tax comparison websites provide valuable insights into how moving might impact your overall financial picture.

Why Is New York State Income Tax Higher Than Some States?

Several factors contribute to New York’s relatively higher income tax rates compared to other states. Chief among them is the state’s extensive network of public services, which requires substantial funding. From world-class educational institutions to cutting-edge healthcare facilities, New York invests heavily in programs benefiting residents across the board.

Additionally, New York City’s high cost of living drives up revenue needs, as many state services are concentrated in urban areas. The state also faces significant infrastructure demands, necessitating ongoing investments in transportation, utilities, and environmental sustainability.

Common Mistakes to Avoid When Filing Your Taxes

Even seasoned taxpayers occasionally make errors when preparing their New York State income tax returns. Avoiding these pitfalls can save time, money, and headaches. One common mistake is failing to update personal information, such as address changes or marital status updates, which can delay processing and refunds.

Another frequent error involves miscalculating deductions or credits. Double-checking figures and consulting reputable resources can prevent costly oversights. Similarly, missing deadlines or submitting incomplete forms can lead to penalties and interest charges. Setting reminders and organizing paperwork well in advance can help ensure timely submission.

Lastly, neglecting to review prior-year returns for potential corrections or amendments can result in lost opportunities for refunds or adjustments. Regular audits of past filings can uncover overlooked deductions or credits, maximizing your financial benefit.

What Happens If I Make a Mistake on My Tax Return?

If you discover an error after filing, don’t panic. The New York State Department of Taxation and Finance provides procedures for correcting mistakes through amended returns. Depending on the nature of the error, you may need to submit Form IT-255 or contact the department directly for guidance.

Common reasons for filing an amendment include:

- Incorrect income reporting

- Missed deductions or credits

- Changes in dependency status

- Mathematical errors

Act promptly to rectify errors, as delays can complicate the resolution process and potentially increase liabilities.

Frequently Asked Questions About New York State Income Tax

1. Can I File My New York State Income Tax Online?

Absolutely! Most taxpayers can file their New York State income tax returns electronically using certified software providers or directly through the Department of Taxation and Finance website. E-filing offers numerous advantages, including faster processing times, reduced error rates, and secure data transmission.

2. Is There a Penalty for Late Filing?

Yes, late filing incurs penalties and interest charges. The penalty for failing to file on time is generally 5% of the unpaid tax for each month or part of a month the return is late, up to a maximum of 25%. Interest accrues at the statutory rate until the balance is paid in full.

3. How Long Should I Keep My Tax Records?

It’s advisable to retain tax records for at least three years from the date you filed your return or the due date, whichever is later. Some experts recommend keeping records for six years or longer, especially if you claim deductions or credits that might attract scrutiny.

Conclusion

Understanding New York State income tax is vital for every resident seeking financial