Taxes are a crucial aspect of living in New York, shaping both personal finances and the state's economy. For residents, business owners, and even tourists, understanding tax in NY is essential for financial planning and compliance. Whether it's income tax, sales tax, property tax, or other levies, the state of New York employs a robust taxation system designed to fund public services, infrastructure, and social programs. However, navigating the intricacies of tax in NY can be daunting, especially with frequent updates and changes in tax laws. This article aims to provide a detailed, user-friendly guide to help you understand and manage your tax obligations effectively.

New York is renowned for its high tax rates compared to many other states, but these taxes support a wide range of services that benefit residents. From world-class healthcare facilities to top-tier educational institutions, the state's tax revenue ensures the maintenance and improvement of essential services. Yet, with so many types of taxes and varying rates depending on location and income levels, it's easy to get overwhelmed. That's why staying informed about tax in NY is more important than ever, whether you're a lifelong resident or new to the state.

As we delve deeper into this comprehensive guide, we will explore the different types of taxes in New York, how they are calculated, and strategies to optimize your tax planning. Additionally, we will address common questions and concerns that arise when dealing with tax in NY, ensuring you have all the information you need to make informed decisions. Let's begin by outlining the key aspects of this article to give you a clear roadmap of what to expect.

Read also:How Safe Is Ullu Webseries Download Movierulz In 2023

Table of Contents

- 1. What Are the Key Types of Tax in NY?

- 2. How Does Income Tax Work in New York?

- 3. Why Is Sales Tax Important for Residents?

- 4. Can Property Tax Be Reduced in New York?

- 5. Business Taxes in New York: What You Need to Know

- 6. Estate and Inheritance Taxes: Understanding the Basics

- 7. Tax Credits and Deductions Available in NY

- 8. Frequently Asked Questions About Tax in NY

What Are the Key Types of Tax in NY?

Tax in NY encompasses a variety of types, each serving a unique purpose in funding the state's operations and services. The primary categories include income tax, sales tax, property tax, and business tax, among others. Understanding these different types is the first step toward effective tax management.

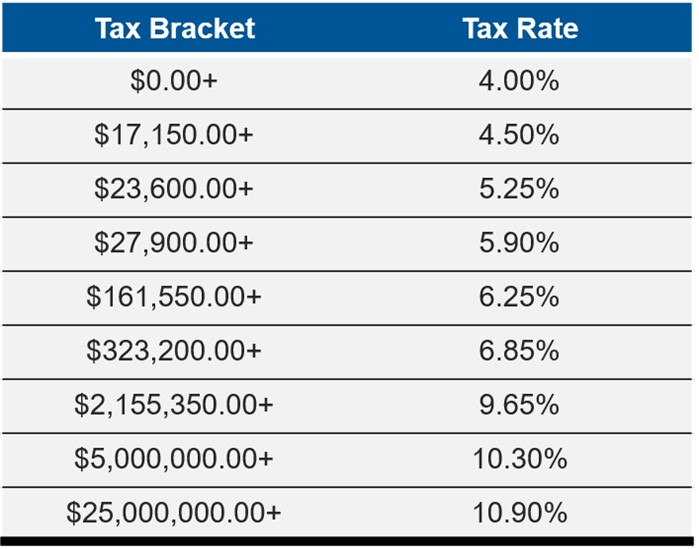

Income Tax: New York State imposes income tax on all its residents, as well as nonresidents who earn income within the state. The tax rate is progressive, meaning it increases as your income rises. For the 2023 tax year, the rates range from 4% to 10.90%, depending on your taxable income bracket. Additionally, New York City residents pay an additional local income tax, making it one of the highest combined rates in the country.

Sales Tax: Sales tax in New York is another significant source of revenue. The state sales tax rate is 4%, but localities can add their own rates, bringing the total rate up to around 8-9% in most areas. Certain items, such as clothing and shoes under $110, are exempt from sales tax, providing some relief to consumers.

Property Tax: Property owners in New York face some of the highest property taxes in the nation. These taxes are levied by local governments and vary widely depending on the location and assessed value of the property. Property taxes fund schools, public safety, and other local services, making them a critical component of the state's fiscal structure.

Business Tax: Businesses operating in New York must also comply with various tax obligations, including corporate income tax, franchise tax, and excise tax. The corporate income tax rate is 6.5%, though certain businesses may qualify for lower rates or exemptions. Proper planning and compliance are essential for businesses to avoid penalties and optimize their financial health.

Why Is Sales Tax Important for Residents?

Sales tax plays a vital role in the financial landscape of New York, impacting residents' daily lives. It is a consumption tax levied on the sale of goods and services, directly affecting how much consumers pay for everyday items. Understanding sales tax is crucial for budgeting and financial planning, as it represents a significant portion of the total cost of purchases.

Read also:Unpacking The Complex Reality Of The Telegram Incest Group Phenomenon A Detailed Analysis

How Sales Tax Affects Consumers: For residents, sales tax means that the final price of goods and services includes an additional percentage based on the item's cost. This can add up quickly, especially for larger purchases like electronics or furniture. However, certain items, such as groceries and prescription medications, are exempt from sales tax, offering some relief to consumers.

Local Variations in Sales Tax: While the state sales tax rate is uniform at 4%, local jurisdictions can impose additional rates, creating variations across the state. For example, New York City has a combined sales tax rate of approximately 8.875%, whereas other areas might have lower rates. Residents should be aware of these differences when shopping or traveling within the state.

Can Property Tax Be Reduced in New York?

Property tax in New York is a substantial financial burden for many homeowners, but there are ways to potentially reduce these costs. By taking advantage of available exemptions, credits, and programs, property owners can lower their tax burden and retain more of their hard-earned money.

Exemptions and Credits: New York offers several property tax relief programs, such as the School Tax Relief (STAR) program, which provides exemptions for homeowners with primary residences. Senior citizens and disabled individuals may also qualify for additional exemptions, depending on their income and circumstances. Applying for these programs requires meeting specific criteria and submitting the necessary documentation.

Appealing Property Assessments: Another strategy for reducing property tax is to challenge the assessed value of your property. If you believe your property has been overvalued, you can file an appeal with your local assessment office. This process involves gathering evidence to support your claim, such as recent property sales in your area or comparable assessments.

How Does Income Tax Work in New York?

Income tax in New York follows a progressive structure, meaning the more you earn, the higher the percentage of your income is taxed. Understanding how this system works is essential for residents and nonresidents alike, as it directly affects your take-home pay and overall financial well-being.

Progressive Tax Rates: As of 2023, New York State income tax rates range from 4% for the lowest income bracket to 10.90% for the highest. These rates are applied to taxable income after deductions and exemptions, making it crucial to optimize your tax planning to minimize your liability. For example, contributing to retirement accounts or taking advantage of tax credits can significantly reduce your taxable income.

Local Income Tax: In addition to state income tax, residents of certain localities, such as New York City, must pay local income tax. The combined rate can exceed 12% for high-income earners, emphasizing the importance of understanding your total tax obligation. Employers typically withhold these taxes from employee paychecks, ensuring compliance and simplifying the process for taxpayers.

Business Taxes in New York: What You Need to Know

Businesses operating in New York face a complex array of tax obligations, requiring careful planning and management to remain compliant and financially healthy. From corporate income tax to franchise tax, understanding these requirements is essential for business success.

Corporate Income Tax: The corporate income tax rate in New York is 6.5%, though certain businesses may qualify for lower rates or exemptions. This tax applies to the net income of corporations doing business in the state, making it a significant expense for many companies. Proper record-keeping and tax planning are crucial for minimizing this liability.

Franchise Tax: In addition to corporate income tax, New York imposes a franchise tax on corporations based on their net worth or net income, whichever is greater. This tax is calculated using a complex formula that considers factors such as capital stock and surplus. Businesses must carefully track their financials to accurately calculate and pay this tax.

Estate and Inheritance Taxes: Understanding the Basics

Estate and inheritance taxes in New York can significantly impact wealth transfer plans, making it essential for individuals to understand these taxes and plan accordingly. These taxes apply to the transfer of assets upon death, affecting both the estate and the beneficiaries.

Estate Tax: New York imposes an estate tax on estates valued above a certain threshold, which changes annually based on inflation adjustments. For 2023, the exemption amount is approximately $6.3 million, meaning estates below this value are exempt from tax. Proper estate planning, such as creating trusts or gifting assets during one's lifetime, can help minimize the impact of estate tax.

Inheritance Tax: Unlike some states, New York does not have a separate inheritance tax. However, beneficiaries may still face tax implications depending on the type of asset received and their relationship to the deceased. Consulting with a tax professional is advisable to ensure compliance and optimize wealth transfer strategies.

Tax Credits and Deductions Available in NY

New York offers a variety of tax credits and deductions designed to reduce the tax burden on residents and businesses. By taking advantage of these opportunities, taxpayers can retain more of their income and improve their financial well-being.

Available Tax Credits: Some of the most common tax credits in New York include the Earned Income Tax Credit (EITC), Child Tax Credit, and Energy Credits. These credits can significantly lower your tax liability, especially for low- and middle-income families. To qualify, taxpayers must meet specific criteria and file the necessary forms.

Popular Deductions: Deductions such as mortgage interest, property taxes, and charitable contributions are also valuable tools for reducing taxable income. By itemizing deductions on your tax return, you can potentially lower your tax bill and increase your refund. However, it's important to weigh the benefits of itemizing against taking the standard deduction to determine the best approach for your situation.

What Are the Most Common Mistakes in Filing Tax in NY?

Filing taxes in New York can be challenging, and mistakes are common, especially for those unfamiliar with the process. Understanding these pitfalls and how to avoid them is crucial for ensuring compliance and maximizing your financial benefits.

Common Errors: Some of the most frequent errors include miscalculating income, failing to claim available credits and deductions, and missing deadlines. These mistakes can lead to penalties, interest charges, and even audits, making it essential to double-check your return before submission. Using tax preparation software or consulting with a professional can help minimize these risks.

How Can I Ensure Compliance with Tax in NY?

Ensuring compliance with tax in NY requires a combination of knowledge, organization, and attention to detail. By staying informed about tax laws, maintaining accurate records, and seeking professional guidance when needed, you can navigate the complexities of New York's tax system with confidence.

Staying Informed: Regularly reviewing updates to tax laws and regulations is essential for remaining compliant. The New York State Department of Taxation and Finance provides resources and updates on their website, making it easier for taxpayers to stay informed. Additionally, subscribing to newsletters or following reputable tax professionals can help you stay up-to-date.

Frequently Asked Questions About Tax in NY

1. Do I Need to Pay Tax in NY If I'm a Nonresident?

Yes, nonresidents who earn income in New York must pay state income tax on that income. The tax rate depends on your income level and is calculated based on the portion of your income earned within the state. Proper documentation and reporting are essential for nonresidents to ensure compliance and avoid penalties.

2. Can I Deduct Property Taxes on My Federal Tax Return?

Yes, you can deduct property taxes paid in New York on your federal tax return, subject to certain limits. The Tax Cuts and Jobs Act (TCJA) caps the deduction for state and local taxes (SALT) at $10,000 per year. This includes property taxes, income taxes, or sales taxes, whichever is applicable. Carefully tracking your payments and consulting with a tax professional can help you maximize this deduction.

3. How Long Should I Keep My Tax Records in NY?

It's generally recommended to keep your tax records for at least three years after filing your return, as this is the statute of limitations for most audits. However, if you've underreported income by 25% or more, the statute extends to six years. For cases involving fraud, there is no statute of limitations. Keeping organized and complete records is crucial for addressing any potential issues that may arise.

Conclusion

Tax in NY is a multifaceted and essential aspect of financial life for residents, businesses, and visitors alike. By understanding the various types of taxes, how they work, and strategies for reducing your liability, you can better manage your finances and achieve your goals. This comprehensive guide has provided detailed insights into income tax, sales tax, property tax, business tax, estate and inheritance taxes, and available credits and deductions. Remember, staying informed and seeking professional guidance when needed are