Residents of New York State face one of the most complex tax systems in the United States, making it crucial to understand how NY state income tax works. As of 2023, the tax rates vary significantly depending on your income bracket, residency status, and filing status. Whether you're a full-time resident, part-year resident, or nonresident, the NY state income tax system requires careful planning and adherence to specific deadlines. With the state's progressive tax structure, understanding your obligations can help you avoid penalties and optimize your financial situation.

NY state income tax is more than just a financial obligation—it's a critical component of fiscal responsibility. The state government uses these funds to support essential services such as education, healthcare, infrastructure, and public safety. For instance, in 2022, the state collected over $100 billion in tax revenue, a significant portion of which came from personal income taxes. This underscores the importance of accurate and timely filings for every taxpayer. Whether you're a freelancer, small business owner, or salaried employee, knowing how the system operates can help you make informed decisions about your finances.

While federal taxes often take center stage during tax season, NY state income tax should not be overlooked. The state imposes its own set of rules, exemptions, and deductions that can significantly impact your overall tax liability. For example, residents can claim certain credits, such as the Empire State Child Credit or the Low-Income Senior and Disabled Exclusion, which can reduce their tax burden. Additionally, the state offers specific tax incentives for homeowners, small businesses, and individuals investing in renewable energy. Understanding these nuances is key to maximizing your tax savings and ensuring compliance with state regulations.

Read also:Discover The Ultimate Entertainment Hub Hd Hub 4 U Com For Seamless Hd Streaming

Table of Contents

- 1. What Is NY State Income Tax?

- 2. How Are Tax Rates Determined for NY State Income Tax?

- 3. Who Must File NY State Income Tax?

- 4. How Do Residency Rules Affect NY State Income Tax?

- 5. What Are the Common Deductions and Credits Available?

- 6. Filing Your NY State Income Tax: Key Steps

- 7. How Can Tax Software Help with NY State Income Tax?

- 8. Frequently Asked Questions

- 9. Conclusion

What Is NY State Income Tax?

NY state income tax refers to the tax levied by the State of New York on the income earned by its residents, businesses, and certain nonresidents. Unlike federal income tax, which applies uniformly across the United States, NY state income tax is governed by the state's unique tax laws and regulations. The tax is calculated based on your taxable income, which is your total income minus any applicable deductions and exemptions. For example, if you earn $100,000 annually and qualify for a $10,000 deduction, your taxable income would be $90,000.

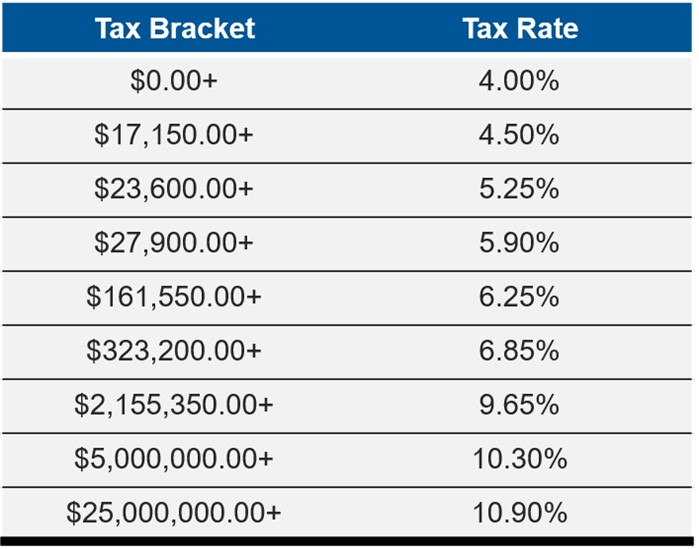

The NY state income tax system operates on a progressive scale, meaning that higher income levels are taxed at higher rates. As of 2023, the tax brackets range from 4% for the lowest income levels to 10.9% for the highest. This ensures that those who earn more contribute a larger share to state revenue. However, the complexity of the system can make it challenging for taxpayers to determine their exact liability without proper guidance. Understanding the basics of NY state income tax is the first step toward ensuring compliance and optimizing your financial strategy.

In addition to individual income tax, the state also imposes taxes on businesses, trusts, and estates. These taxes are calculated differently and often require specialized knowledge to navigate. For instance, corporations operating in New York must file separate tax returns and may be subject to additional taxes, such as the Metropolitan Commuter Transportation District Surcharge. This highlights the importance of consulting a tax professional or utilizing reliable tax software when preparing your NY state income tax return.

How Are Tax Rates Determined for NY State Income Tax?

Tax rates for NY state income tax are determined by a combination of factors, including your income level, filing status, and residency status. The state uses a progressive tax system, which means that as your income increases, so does your tax rate. For example, individuals earning less than $8,500 are taxed at 4%, while those earning over $1,077,550 are taxed at 10.9%. This ensures that higher-income individuals contribute a larger share to state revenue without placing an undue burden on lower-income taxpayers.

Additionally, your filing status plays a crucial role in determining your tax rate. Single filers, married couples filing jointly, and heads of households all have different tax brackets and thresholds. For instance, a married couple filing jointly may qualify for a higher exemption amount than a single filer, reducing their overall tax liability. Furthermore, part-year residents and nonresidents are subject to different rules, which can affect their tax rates and obligations. Understanding these distinctions is essential for accurately calculating your NY state income tax.

Residency status is another key factor in determining tax rates. Full-time residents are taxed on all their income, regardless of where it was earned, while part-year residents are taxed only on income earned within the state. Nonresidents, on the other hand, are taxed only on income sourced from New York. This complexity underscores the importance of accurate record-keeping and thorough documentation when filing your NY state income tax return.

Read also:The Ultimate Guide To The Best Ssh Remote Iot Device Raspberry Pi For Beginners

Who Must File NY State Income Tax?

Not everyone is required to file a NY state income tax return, but understanding the rules can help you avoid penalties and ensure compliance. Generally, you must file if your income exceeds the standard deduction for your filing status. For example, a single filer with no dependents must file if their income exceeds $8,500, while a married couple filing jointly must file if their combined income exceeds $17,000. These thresholds are adjusted annually to account for inflation and changes in state tax laws.

In addition to income thresholds, certain credits and deductions may require you to file a return, even if your income is below the filing requirement. For instance, if you qualify for the Empire State Child Credit or the Low-Income Senior and Disabled Exclusion, you must file a return to claim these benefits. Similarly, if you received a refundable credit or made estimated tax payments during the year, filing a return is necessary to claim your refund.

It's also important to note that part-year residents and nonresidents may have different filing requirements. Part-year residents are required to file if they earned income in New York during their period of residency, while nonresidents must file if they earned income sourced from the state. These rules ensure that all individuals contributing to the state's economy are appropriately taxed, regardless of their residency status.

How Do Residency Rules Affect NY State Income Tax?

Residency rules play a critical role in determining your NY state income tax obligations. The state distinguishes between full-time residents, part-year residents, and nonresidents, each with its own set of requirements and benefits. Full-time residents are taxed on all their income, regardless of where it was earned, while part-year residents are taxed only on income earned within the state. Nonresidents, on the other hand, are taxed only on income sourced from New York, such as wages from a New York-based employer or rental income from property located in the state.

Determining your residency status can be complex, especially if you spend significant time in multiple states. The state uses a "183-day rule" to determine residency, meaning that if you spend more than half the year in New York, you are considered a full-time resident. However, exceptions exist for individuals who maintain a permanent home in another state and spend less than 30 days in New York. These nuances highlight the importance of careful planning and documentation when managing your tax obligations.

Residency rules also affect your eligibility for certain credits and deductions. For example, full-time residents may qualify for the Low-Income Senior and Disabled Exclusion, which reduces their taxable income, while part-year residents and nonresidents may not. Understanding these distinctions can help you optimize your tax strategy and ensure compliance with state regulations. Consulting a tax professional or utilizing reliable tax software can provide additional guidance and peace of mind during the filing process.

What Are the Common Deductions and Credits Available?

NY state income tax offers a variety of deductions and credits designed to reduce your taxable income and lower your overall tax liability. Some of the most common deductions include the standard deduction, itemized deductions, and personal exemptions. For example, single filers can claim a standard deduction of $8,500, while married couples filing jointly can claim $17,000. Alternatively, taxpayers can itemize their deductions, which may include mortgage interest, charitable contributions, and medical expenses exceeding a certain threshold.

In addition to deductions, the state offers several credits to help taxpayers reduce their tax burden. The Empire State Child Credit, for instance, provides a refundable credit of up to $1,050 per qualifying child, depending on your income level. The Low-Income Senior and Disabled Exclusion allows eligible taxpayers to exclude up to $20,000 of retirement income from taxation. Furthermore, the Child and Dependent Care Credit can help offset the cost of childcare, making it easier for working families to manage their expenses.

Business owners and investors may also qualify for specific deductions and credits, such as the Small Business Credit or the Renewable Energy Credit. These incentives encourage economic growth and innovation while providing tax relief to qualifying individuals and organizations. Understanding the available deductions and credits can help you maximize your tax savings and ensure compliance with NY state income tax regulations.

Filing Your NY State Income Tax: Key Steps

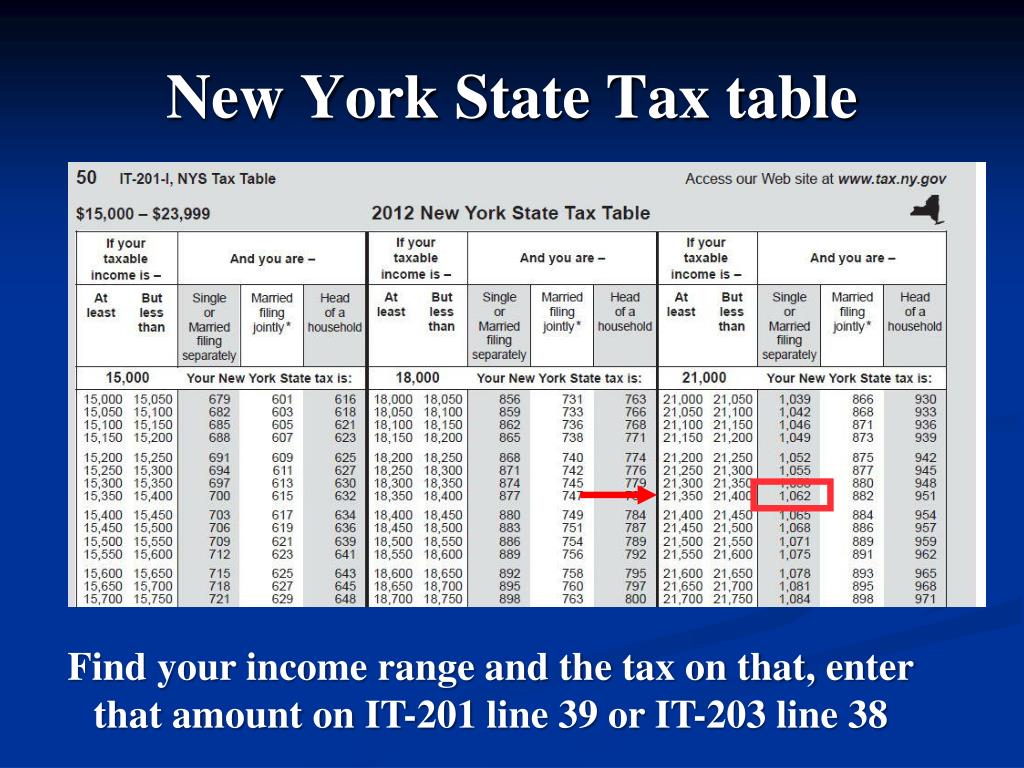

Filing your NY state income tax return involves several key steps, each of which is crucial for ensuring accuracy and compliance. The process begins with gathering all necessary documents, including your W-2 forms, 1099s, and any other records of income earned during the year. Once you have compiled this information, you can choose to file your return electronically or by mail. Electronic filing is generally faster and more secure, offering additional benefits such as direct deposit of your refund and automatic error checking.

When preparing your return, it's important to choose the correct filing status and ensure that all information is accurate and up-to-date. This includes your Social Security number, address, and any dependents you are claiming. If you itemize your deductions, you must provide supporting documentation for each expense, such as receipts or bank statements. Additionally, if you qualify for any credits or exclusions, you must complete the appropriate forms and attach any required documentation.

After submitting your return, it's essential to monitor its status and address any issues that may arise. The New York State Department of Taxation and Finance provides an online tool for tracking your return and checking the status of your refund. If you owe additional taxes, you can pay online or by mail, ensuring that your payment is received by the due date to avoid penalties and interest. Following these steps can help you navigate the filing process with confidence and ease.

How Can Tax Software Help with NY State Income Tax?

Tax software has become an invaluable tool for individuals and businesses seeking to simplify the NY state income tax filing process. These programs offer a range of features designed to streamline the process, from automatically calculating your tax liability to identifying potential deductions and credits. Popular options like TurboTax, H&R Block, and TaxSlayer provide user-friendly interfaces and step-by-step guidance, making it easier for taxpayers to prepare and file their returns accurately and efficiently.

One of the key benefits of tax software is its ability to update automatically with the latest tax laws and regulations. This ensures that you are always working with the most current information, reducing the risk of errors and penalties. Additionally, many programs offer state-specific features, such as pre-filled forms and state-specific credits, which can further simplify the filing process for NY state income tax. For example, TurboTax offers a state-specific module that includes forms like IT-201 and IT-2105, ensuring that you meet all state requirements.

Tax software also provides valuable tools for tracking your financial information throughout the year, helping you stay organized and prepared for tax season. Features like expense trackers, receipt scanners, and investment trackers can make it easier to gather the necessary documentation and maximize your deductions. Furthermore, many programs offer live support and consultation services, providing additional assistance for complex tax situations or questions about NY state income tax. By leveraging these resources, you can save time, reduce stress, and ensure compliance with state regulations.