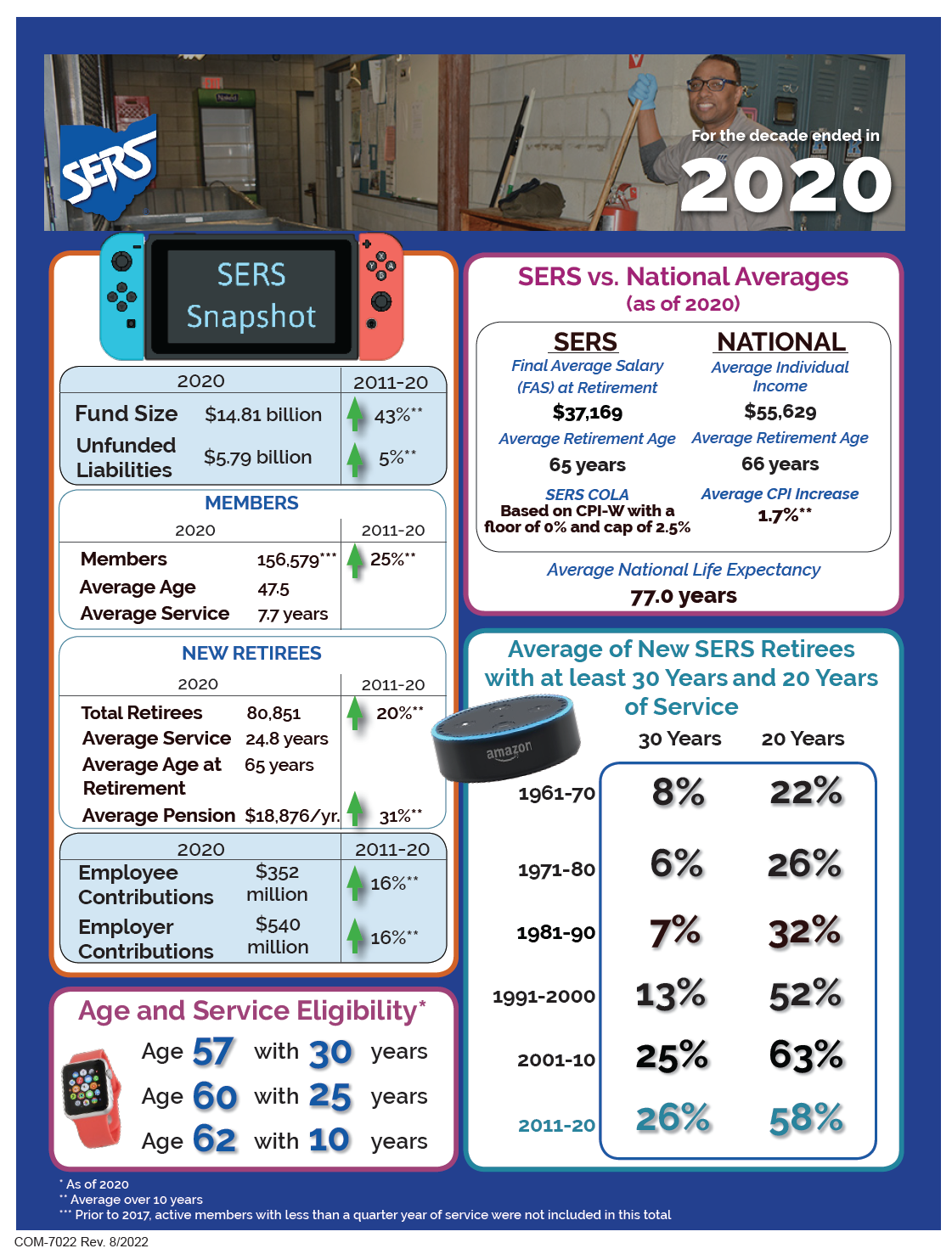

The State Employees Retirement System of Ohio, commonly referred to as SERS of Ohio, is a cornerstone of financial stability for thousands of public servants across the state. Established to provide retirement benefits, healthcare coverage, and other essential financial services, SERS of Ohio plays an indispensable role in ensuring that Ohio’s workforce can retire with dignity and security. For those unfamiliar with its intricate workings, understanding SERS of Ohio is not just beneficial—it’s essential for anyone planning their future in public service. This article delves deep into the system, unraveling its complexities while offering actionable insights to help you make the most of your benefits.

As the needs of Ohio's public sector employees evolve, so does SERS of Ohio. From adjusting contribution rates to expanding benefit options, the system continually adapts to meet the demands of its members. Whether you're a newly hired state employee, a seasoned veteran nearing retirement, or simply someone curious about retirement planning, this guide will equip you with the knowledge to navigate the system effectively. By exploring topics such as eligibility criteria, contribution structures, and withdrawal options, we aim to demystify SERS of Ohio and empower you to take control of your financial future.

In today's rapidly changing economic landscape, securing a stable retirement is more important than ever. SERS of Ohio offers a robust framework for achieving that goal, but it requires proactive engagement and informed decision-making. This article is your roadmap to understanding the nuances of the system, maximizing your benefits, and ensuring a financially secure retirement. Let’s dive in and uncover everything you need to know about SERS of Ohio.

Read also:Unveiling The Allure Of Lara Rose Erome A Rising Star In The Spotlight

Table of Contents

- 1. What Are the Eligibility Requirements for SERS of Ohio?

- 2. Understanding the Contribution Structure of SERS of Ohio

- 3. How Does SERS of Ohio Calculate Retirement Benefits?

- 4. Can SERS of Ohio Members Withdraw Funds Early?

- 5. Exploring Health Benefits Offered by SERS of Ohio

- 6. Maximizing Your SERS of Ohio Benefits

- 7. The Role of SERS of Ohio in Long-Term Financial Planning

- 8. Frequently Asked Questions About SERS of Ohio

What Are the Eligibility Requirements for SERS of Ohio?

Eligibility for SERS of Ohio is a critical factor that determines whether you can participate in the system and enjoy its benefits. To qualify, individuals must be employed by a participating public entity in Ohio. This includes state agencies, universities, community colleges, and certain other organizations designated by the system. Membership is automatic for most employees upon hire, provided they meet the employment criteria set forth by their employer and SERS of Ohio.

One of the primary eligibility factors is the type of employment. Full-time, part-time, and seasonal employees may all qualify for SERS of Ohio, depending on the specifics of their employment contract and the number of hours worked. For instance, part-time employees who work at least 20 hours per week or accumulate a certain number of service hours annually are typically eligible. Additionally, individuals transitioning from one eligible position to another within the same employer may retain their membership status without interruption.

Another important consideration is the length of service. While some benefits, such as healthcare, may be available immediately upon enrollment, others, like retirement benefits, require a minimum period of service. For retirement eligibility, members must typically accumulate five years of credited service. However, certain exceptions exist, such as for employees who leave the workforce before reaching this milestone. These exceptions often involve partial refunds of contributions or alternative benefit options.

Are There Age Restrictions for SERS of Ohio Membership?

Age is another factor that influences SERS of Ohio eligibility. While there is no specific age requirement for joining the system, retirement benefits are subject to age-based restrictions. Members must reach a certain age, known as the "normal retirement age," to access full retirement benefits without penalties. This age varies depending on when the individual joined the system and their birth year. For example, those hired after January 1, 2013, must generally reach age 67 to qualify for full benefits.

Understanding these eligibility requirements is crucial for planning your career and retirement effectively. By familiarizing yourself with the rules governing membership, you can ensure that you meet all necessary criteria and avoid potential pitfalls that could impact your benefits.

Read also:Dirty Dr Pepper Sonic The Ultimate Guide To A Sweet And Salty Sensation

Understanding the Contribution Structure of SERS of Ohio

Contributions are the backbone of SERS of Ohio, forming the financial foundation upon which all benefits are built. Members contribute a percentage of their earnings to the system, with the rate determined by their employment category and hire date. As of the latest updates, the standard contribution rate for most employees is 10% of their gross salary. However, this rate may vary slightly depending on individual circumstances and any changes enacted by the legislature.

In addition to employee contributions, employers also contribute to the system. These employer contributions help ensure the long-term sustainability of SERS of Ohio by covering the costs associated with benefit payouts. The exact contribution rate for employers is calculated based on actuarial projections and financial health assessments of the system. While members do not directly influence these rates, they benefit indirectly from a well-funded retirement system.

It’s worth noting that contributions are mandatory for all eligible employees. Once enrolled, members are required to continue making contributions throughout their employment, barring specific exceptions such as approved leaves of absence or terminations. These contributions are deducted automatically from paychecks, ensuring consistent funding for the system.

How Do Contributions Impact Retirement Benefits?

The relationship between contributions and retirement benefits is direct and significant. The more you contribute to SERS of Ohio during your working years, the greater your potential retirement benefits will be. Contributions are used to calculate your final average salary, which is a key component in determining your monthly retirement payment. This final average salary is typically based on your highest consecutive years of earnings, further emphasizing the importance of consistent contributions over time.

Additionally, members have the option to make voluntary supplemental contributions, which can enhance their retirement benefits beyond the standard payout. These supplemental contributions are not mandatory but offer an opportunity for members to increase their financial security in retirement. By exploring all available contribution options, you can optimize your benefits and better prepare for the future.

How Does SERS of Ohio Calculate Retirement Benefits?

Calculating retirement benefits under SERS of Ohio involves a detailed formula that takes into account several key factors. At its core, the formula considers three primary elements: your final average salary, your years of credited service, and a benefit multiplier. Each of these components plays a critical role in determining the amount of your monthly retirement payment.

The final average salary is calculated by averaging your highest consecutive years of earnings. For most members, this period spans three to five years, depending on when they joined the system and their specific employment category. By focusing on your highest earnings, the system ensures that your retirement benefits reflect your peak earning potential during your career.

Years of credited service refer to the total amount of time you have worked in an eligible position while contributing to SERS of Ohio. Each year of service accrues additional benefits, with longer service resulting in higher monthly payments. It’s important to note that not all periods of employment are eligible for credited service, so understanding the rules governing service accrual is essential.

What Is the Role of the Benefit Multiplier?

The benefit multiplier is a percentage applied to your final average salary and years of credited service to determine your monthly benefit. For most members, the standard multiplier is 1.7%, though this rate may vary depending on your hire date and membership category. For example, if you have a final average salary of $50,000 and 20 years of credited service, your monthly benefit would be calculated as follows: ($50,000 x 20 x 1.7%) ÷ 12 = $1,416.67 per month.

This formula underscores the importance of maximizing your contributions and years of service. By increasing your final average salary or extending your credited service, you can significantly enhance your retirement benefits. Understanding how the calculation works allows you to plan effectively and make informed decisions about your career trajectory and retirement goals.

Can SERS of Ohio Members Withdraw Funds Early?

Early withdrawal of funds from SERS of Ohio is a topic of considerable interest for many members, particularly those facing unexpected financial challenges or life changes. While the system is designed to provide long-term retirement security, provisions exist for accessing funds before reaching retirement age. However, these options come with significant restrictions and potential penalties, making it essential to carefully evaluate your circumstances before proceeding.

One of the most common early withdrawal options is the deferred vested benefit. This option allows members who leave public employment before reaching retirement age to receive a reduced monthly benefit starting at age 55. While this provides some financial relief, the reduction in benefits can be substantial, so it’s important to weigh the long-term impact on your retirement security.

Another option is the refund of contributions. Members who terminate employment and choose not to remain in the system can request a refund of their contributions, though this typically excludes any interest or employer contributions. Refunds are subject to federal income tax and may incur additional penalties if taken before age 59½. Additionally, opting for a refund means forfeiting all future retirement benefits, so this choice should be made with extreme caution.

Are There Exceptions for Hardship Withdrawals?

In limited cases, SERS of Ohio may allow hardship withdrawals for members facing severe financial difficulties. These withdrawals are subject to strict criteria and require documentation of the hardship. Examples of qualifying hardships include medical emergencies, catastrophic losses, or other unforeseen circumstances that create an immediate and critical financial need. While hardship withdrawals can provide temporary relief, they also carry tax implications and may reduce future benefits, so they should only be pursued as a last resort.

Before considering any form of early withdrawal, it’s advisable to consult with a financial advisor or SERS of Ohio representative to fully understand the implications and explore alternative solutions. By making informed decisions, you can protect your long-term financial well-being while addressing immediate needs.

Exploring Health Benefits Offered by SERS of Ohio

In addition to retirement benefits, SERS of Ohio offers comprehensive health coverage options designed to support members throughout their careers and into retirement. These benefits include medical, dental, vision, and prescription drug coverage, providing a safety net for both active employees and retirees. The system partners with leading insurance providers to deliver high-quality care at competitive rates, ensuring that members have access to the services they need.

For active employees, health benefits are typically available immediately upon enrollment, with premiums deducted from paychecks. The specific plans offered may vary depending on the employer and membership category, so it’s important to review your options carefully during open enrollment periods. Many plans include preventive care services at no additional cost, encouraging members to prioritize their health and well-being.

Retirees also have access to health benefits through SERS of Ohio, though these benefits may be subject to eligibility requirements and cost-sharing arrangements. Retiree health coverage is particularly valuable for those not yet eligible for Medicare, as it bridges the gap between employment and federal health insurance programs. By planning ahead and understanding the available options, retirees can ensure they have the coverage they need to maintain their quality of life.

Maximizing Your SERS of Ohio Benefits

To get the most out of SERS of Ohio, it’s essential to adopt a proactive approach to managing your benefits. This involves understanding the system’s rules and regulations, taking advantage of available resources, and making strategic decisions about your contributions and retirement planning. By following these best practices, you can optimize your benefits and secure a more stable financial future.

1. Stay Informed About System Changes

SERS of Ohio regularly updates its policies and procedures to reflect changing economic conditions and legislative priorities. Staying informed about these changes ensures that you remain compliant with the system’s requirements and can adapt your strategies accordingly. Regularly review updates from SERS of Ohio, attend informational sessions, and consult with advisors to stay ahead of any potential impacts.

2. Maximize Your Contributions

As discussed earlier, contributions directly influence your retirement benefits. By maximizing your contributions, you can enhance your final average salary and years of credited service, leading to higher monthly payments in retirement. Consider taking advantage of supplemental contribution options and exploring employer matching programs, if available, to further boost your savings.

3. Plan for the Long Term

Effective retirement planning requires a long-term perspective. Work with financial advisors to develop a comprehensive plan that aligns with your goals and incorporates SERS of Ohio benefits. This plan should address not only your retirement income needs but also other aspects of financial security, such as healthcare costs, inflation, and unexpected expenses.

The Role of SERS of Ohio in Long-Term Financial Planning

SERS of Ohio serves as a cornerstone of long-term financial planning for Ohio’s public sector employees. By providing a reliable source of retirement income and comprehensive health coverage, the system helps members achieve financial independence and peace of mind. However, its role extends beyond mere benefit provision; it also fosters a culture of financial literacy and responsibility among its members.

Through educational programs, online resources, and personalized counseling, SERS of Ohio empowers members to make informed decisions about their financial futures. This support is invaluable in navigating the complexities of retirement planning, ensuring that members are prepared for the challenges and