Tax New York is one of the most crucial aspects of financial management for residents, businesses, and visitors alike. The state’s tax system is intricate, with numerous regulations, rates, and deadlines that can be overwhelming for those unfamiliar with the process. From income taxes to sales taxes, understanding how these systems work is essential for anyone looking to comply with state laws while optimizing their financial strategies. Whether you're a new resident or an experienced business owner, this guide will provide you with the knowledge and tools needed to navigate the complexities of New York's tax landscape effectively.

As one of the most populous and economically vibrant states in the U.S., New York imposes a range of taxes that contribute significantly to its revenue. These taxes are designed to fund public services, infrastructure, and social programs that benefit residents and businesses. However, the state's tax structure is not without its challenges. With varying rates depending on location, income level, and type of transaction, it's easy to get lost in the details. This article aims to demystify the complexities of Tax New York, offering clear explanations and actionable insights for taxpayers.

By exploring the various types of taxes levied in New York, their implications, and strategies for compliance, you'll gain a deeper understanding of how to manage your finances responsibly. From navigating individual income taxes to understanding property and sales taxes, this guide will equip you with the information necessary to make informed decisions. Let's dive into the world of Tax New York and discover how you can stay ahead of the curve.

Read also:Elaine Dratch The Woman Behind The Laughter

Table of Contents

- 1. What Are the Key Components of Tax New York?

- 2. How Does Tax New York Impact Residents and Businesses?

- 3. Why Is Understanding Tax New York Important for Financial Planning?

- 4. How Much Does Tax New York Cost You?

- 5. What Are the Deadlines for Filing Tax New York?

- 6. Common Misconceptions About Tax New York

- 7. Tax New York: Strategies for Minimizing Your Liability

- 8. Frequently Asked Questions About Tax New York

What Are the Key Components of Tax New York?

Tax New York encompasses several types of taxes that residents and businesses must navigate. The primary components include individual income tax, corporate income tax, sales tax, property tax, and excise tax. Each of these taxes serves a specific purpose and has its own set of rules and regulations.

Individual income tax is perhaps the most well-known component of Tax New York. It applies to all residents and nonresidents who earn income within the state. The tax rates vary depending on the taxpayer's income level, with higher earners paying a larger percentage of their income. In addition to the state-level income tax, many cities and counties in New York impose their own local income taxes, further complicating the process.

Corporate income tax is another critical component, affecting businesses operating within the state. The rates for corporate taxes are generally higher than those for individuals, reflecting the larger revenue streams generated by businesses. Sales tax, on the other hand, applies to most goods and services purchased in New York, with rates varying by county. Property tax is levied on real estate, while excise taxes target specific goods like alcohol, tobacco, and gasoline.

Why Is Individual Income Tax So Important?

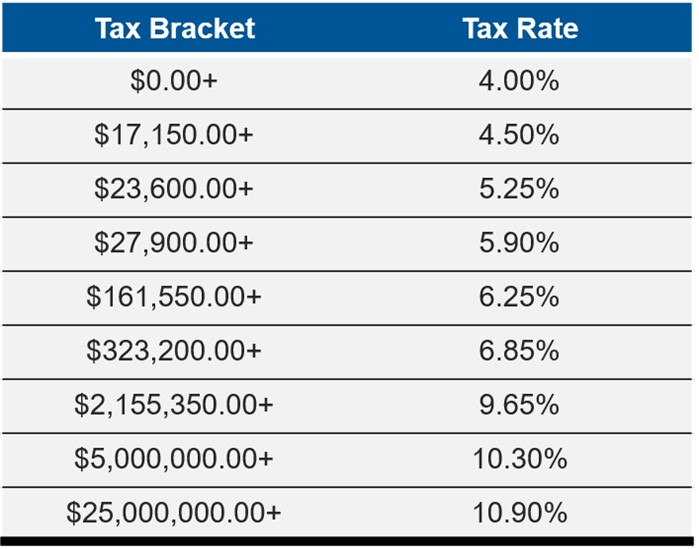

Individual income tax is the backbone of Tax New York, generating a significant portion of the state's revenue. It is calculated based on a taxpayer's adjusted gross income (AGI) and is subject to progressive tax rates. For example, as of 2023, the lowest tax rate is 4%, while the highest rate for high-income earners is 8.82%. This structure ensures that those who earn more contribute a larger share to the state's coffers.

Moreover, individual income tax plays a vital role in funding essential services such as education, healthcare, and public safety. By understanding how this tax works, residents can better plan their finances and ensure compliance with state regulations. Additionally, being aware of deductions and credits available under the state's tax code can help reduce your overall tax liability.

How Does Sales Tax Work in New York?

Sales tax in New York is a consumption-based tax levied on the sale of goods and services. The state sales tax rate is 4%, but local jurisdictions can add their own rates, bringing the total sales tax rate to as high as 8.45% in some areas. Certain items, such as clothing and shoes costing less than $110, are exempt from sales tax, providing relief to consumers.

Read also:Unveiling The Power Of Son385 A Comprehensive Guide To Its Applications And Benefits

Businesses must collect sales tax on behalf of the state and remit it to the New York State Department of Taxation and Finance. Failure to comply with these requirements can result in penalties and interest charges. Therefore, it's crucial for businesses to stay informed about the latest sales tax regulations and implement appropriate systems for collecting and reporting taxes.

How Does Tax New York Impact Residents and Businesses?

Tax New York has far-reaching implications for both residents and businesses. For individuals, taxes affect disposable income, savings, and investment opportunities. High tax rates can reduce take-home pay, making it challenging for some families to meet their financial obligations. On the other hand, businesses must contend with corporate income taxes, payroll taxes, and sales taxes, all of which impact profitability and growth.

Residents who own property must also consider property taxes, which can be substantial depending on the location and value of the property. These taxes are used to fund local services such as schools, libraries, and public safety initiatives. Understanding how property taxes are assessed and appealing unfair assessments can help homeowners manage their expenses more effectively.

What Challenges Do Businesses Face with Tax New York?

Businesses operating in New York face unique challenges when it comes to taxation. In addition to corporate income taxes, they must navigate payroll taxes, sales taxes, and other compliance requirements. The complexity of the tax code can make it difficult for small businesses, in particular, to remain compliant without incurring additional costs for professional tax services.

Furthermore, the state's tax policies can influence business decisions, such as where to locate operations or whether to expand. High tax burdens may deter companies from investing in New York, potentially stifling economic growth. However, businesses that understand the tax landscape and take advantage of available incentives and credits can position themselves for success in the competitive New York market.

Why Is Understanding Tax New York Important for Financial Planning?

Understanding Tax New York is crucial for effective financial planning. Whether you're an individual managing personal finances or a business owner overseeing a company's operations, having a clear grasp of tax obligations and opportunities can lead to better decision-making. By staying informed about tax laws and regulations, you can identify strategies to minimize your tax liability and maximize your financial resources.

For example, knowing which deductions and credits are available under the state's tax code can help reduce your taxable income. This knowledge can lead to significant savings over time, allowing you to allocate more resources toward savings, investments, or other financial goals. Additionally, being aware of upcoming changes to the tax code can help you adjust your strategies accordingly, ensuring continued compliance and financial stability.

How Can Tax Planning Improve Your Financial Situation?

Tax planning involves analyzing your financial situation and implementing strategies to optimize your tax position. By taking a proactive approach to tax planning, you can identify areas where you can reduce your tax burden and increase your after-tax income. This might include contributing to retirement accounts, taking advantage of tax credits, or timing certain transactions to occur in years with lower income levels.

For businesses, tax planning can involve structuring operations to minimize taxable income, investing in tax-advantaged assets, or utilizing tax deferral strategies. Effective tax planning requires a thorough understanding of Tax New York and a willingness to adapt to changing circumstances. With the right strategies in place, you can enhance your financial well-being and achieve your long-term goals.

How Much Does Tax New York Cost You?

The cost of Tax New York varies depending on several factors, including your income level, the type of property you own, and the nature of your business activities. For individuals, income taxes are the most significant expense, with rates ranging from 4% to 8.82% depending on your AGI. Property taxes can also be substantial, particularly in areas with high property values.

Businesses face additional costs in the form of corporate income taxes, payroll taxes, and sales taxes. These taxes can add up quickly, especially for companies with large operations or significant revenue streams. Understanding the total cost of Tax New York is essential for budgeting and financial planning, as it allows you to allocate resources more effectively and avoid unexpected expenses.

What Are the Average Tax Rates in New York?

The average tax rates in New York depend on the type of tax being assessed. For individual income taxes, the average rate is around 6%, though this can vary widely based on income level. Property taxes, on the other hand, are assessed as a percentage of the property's assessed value, with rates varying by location. In some areas, property tax rates can exceed 2% of the property's value, making them a significant expense for homeowners.

Sales tax rates in New York average around 7%, though this can vary depending on the county and the specific goods or services being purchased. Businesses must also consider payroll taxes, which include unemployment insurance taxes and Social Security and Medicare contributions. These taxes can add up to several percentage points of a company's payroll expenses, further impacting profitability.

What Are the Deadlines for Filing Tax New York?

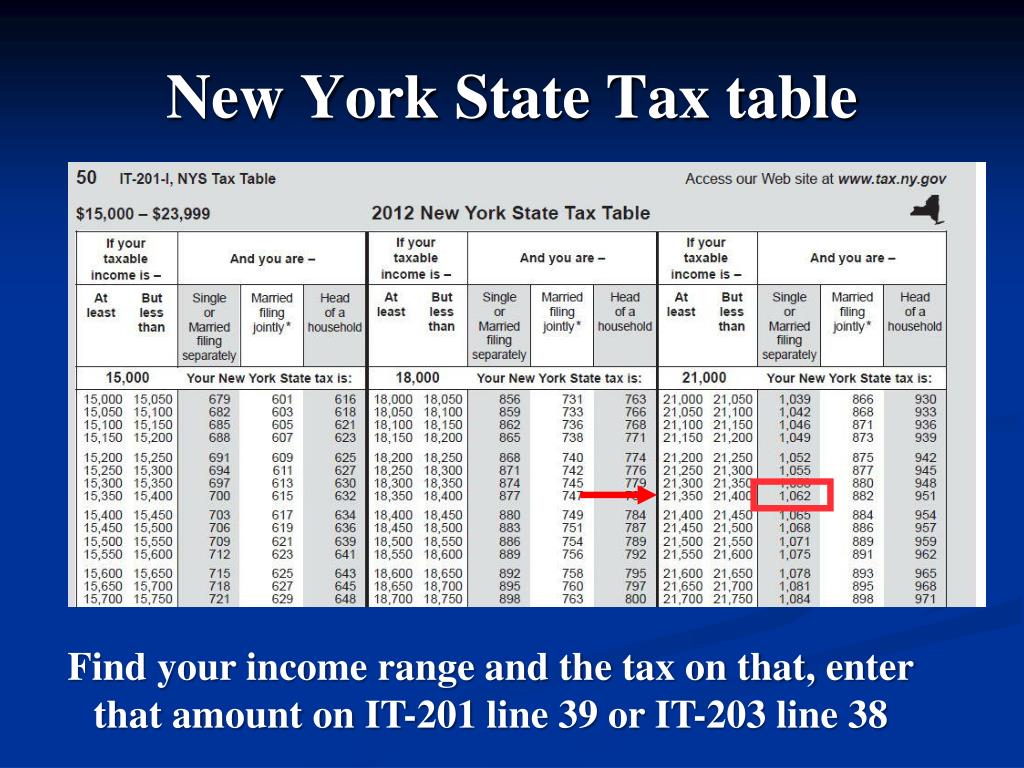

Filing deadlines for Tax New York depend on the type of tax being reported. For individual income taxes, the deadline is typically April 15th of each year, though extensions can be requested if needed. Corporate income taxes generally have the same deadline, though businesses with fiscal year-end dates may have different reporting schedules.

Property tax deadlines vary by jurisdiction, with some areas requiring payments twice a year while others allow for quarterly installments. Sales tax returns must be filed monthly, quarterly, or annually, depending on the business's sales volume and the local tax authority's requirements. Staying on top of these deadlines is crucial for avoiding penalties and interest charges, which can quickly add up if payments are late.

How Can You Avoid Missing Tax Deadlines?

Missing tax deadlines can result in penalties, interest charges, and other negative consequences. To avoid these issues, it's important to establish a system for tracking deadlines and submitting required documents on time. This might include setting reminders, using tax preparation software, or working with a professional accountant to ensure compliance.

For businesses, automating tax processes can help streamline reporting and payment activities, reducing the risk of missed deadlines. Additionally, staying informed about changes to tax laws and regulations can help you adjust your strategies accordingly, ensuring continued compliance and financial stability.

Common Misconceptions About Tax New York

There are several common misconceptions about Tax New York that can lead to confusion and errors. One of the most prevalent myths is that all residents pay the same tax rates, which is not true due to the progressive nature of the state's income tax system. Another misconception is that property taxes are fixed, when in reality, they can fluctuate based on changes in property values and local tax rates.

Some people also believe that sales tax applies to all goods and services, but certain items, such as groceries and prescription medications, are exempt. Understanding these nuances is essential for accurate tax reporting and compliance. By dispelling these myths and gaining a deeper understanding of Tax New York, you can make more informed decisions about your finances.

Tax New York: Strategies for Minimizing Your Liability

Minimizing your tax liability under Tax New York requires a combination of knowledge, planning, and action. One effective strategy is to take full advantage of available deductions and credits, such as those for mortgage interest, charitable contributions, and energy-efficient home improvements. Another approach is to time certain transactions, such as selling investments, to occur in years with lower income levels, thereby reducing your taxable income.

For businesses, strategies might include restructuring operations to minimize taxable income, investing in tax-advantaged assets, or utilizing tax deferral strategies. Working with a qualified tax professional can help you identify additional opportunities to reduce your tax burden and enhance your financial well-being. By implementing these strategies, you can optimize your tax position and achieve your financial goals more effectively.

Frequently Asked Questions About Tax New York

What Happens If You Miss a Tax Deadline?

If you miss a tax deadline, you may incur penalties and interest charges, which can add up quickly. To avoid these consequences, it's important to file your taxes on time or request an extension if needed. In some cases, the state may offer relief programs for taxpayers who experience hardship or other extenuating circumstances.

Can You Appeal a Property Tax Assessment?

Yes, you can appeal a property tax assessment if you believe it is unfair or inaccurate. The process typically involves submitting a formal appeal to the local tax authority and providing evidence to support your claim. If successful, the appeal could result in a reduction of your property tax bill, providing relief to homeowners facing financial challenges.

Conclusion

Tax New York is a complex but essential aspect of financial management for residents and businesses in the state. By understanding the various components of the tax system, their implications, and strategies for compliance, you can navigate the complexities of taxation more effectively. Whether you're