NY income tax is a critical aspect of financial management for residents of the Empire State. Whether you're a new resident, a long-time New Yorker, or a business owner, understanding the intricacies of New York's tax system is essential for maximizing your financial health. The state of New York imposes a progressive income tax structure, meaning the more you earn, the higher the tax rate you may face. This tax system is designed to fund essential public services, infrastructure, and programs that benefit all New Yorkers. However, navigating the complexities of NY income tax can be challenging without proper guidance.

For many individuals and businesses, NY income tax represents one of the largest annual expenses. It's crucial to stay informed about tax laws, exemptions, deductions, and credits to ensure compliance and optimize your tax liability. In addition to federal income taxes, New York residents must also account for state and, in some cases, local taxes. Understanding the differences between these tax layers and how they interact is vital for effective financial planning. This article aims to demystify NY income tax and provide actionable insights to help you make informed decisions.

As we delve deeper into the topic, you'll discover key aspects of NY income tax, including how it's calculated, available deductions and credits, and strategies for reducing your tax burden. By the end of this guide, you'll have a comprehensive understanding of New York's tax system and how it impacts your financial situation. Whether you're filing your taxes independently or working with a professional, this knowledge will empower you to take control of your finances and plan for the future.

Read also:Unlocking The Potential Of Sone436 A Comprehensive Guide For The Future

Table of Contents

- What Is NY Income Tax?

- NY Income Tax Rates: How Much Do You Pay?

- Exploring NY Income Tax Deductions and Credits

- How Do You File NY Income Tax?

- Why Does Local NY Income Tax Matter?

- How Can You Reduce Your NY Income Tax?

- What Impact Does NY Income Tax Have on Your Finances?

- Where Is NY Income Tax Headed in the Future?

- Frequently Asked Questions About NY Income Tax

What Is NY Income Tax?

NY income tax refers to the state-imposed tax on the income earned by individuals, businesses, and other entities residing or operating within New York State. This tax is a significant source of revenue for the state, funding critical services such as education, healthcare, transportation, and public safety. Unlike federal income tax, which is uniform across the United States, NY income tax rates vary depending on your income level, filing status, and location within the state.

The NY income tax system operates on a progressive scale, meaning higher earners pay a larger percentage of their income in taxes compared to lower-income individuals. This structure aims to create a fairer tax burden, ensuring those with greater financial resources contribute proportionally more to support the state's infrastructure and services. Additionally, certain deductions and credits are available to help reduce your taxable income and lower your overall tax liability.

In addition to state income tax, residents of specific municipalities within New York may also be subject to local income taxes. These local taxes are typically lower than the state tax but can add up over time, especially for residents living in high-tax areas like New York City. Understanding both state and local tax obligations is essential for accurate financial planning and compliance with tax laws.

NY Income Tax Rates: How Much Do You Pay?

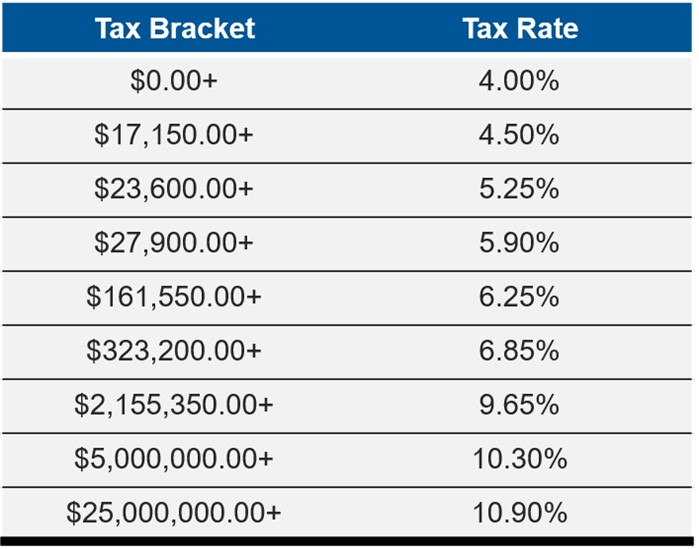

NY income tax rates are structured in a progressive manner, with seven distinct tax brackets as of the latest tax year. These brackets are designed to ensure that individuals and families pay a fair share based on their income level. For example, single filers earning up to $8,500 are taxed at the lowest rate of 4%, while those earning over $250,000 may face a top marginal rate of 8.82%. It's important to note that these rates are subject to change annually, depending on legislative updates and economic conditions.

For married couples filing jointly, the tax brackets are slightly higher, reflecting the combined income of both spouses. This adjustment aims to accommodate the financial realities of dual-income households and ensure equitable treatment under the tax code. Additionally, New York offers a variety of deductions and credits that can further reduce your taxable income, potentially lowering your effective tax rate.

Here's a breakdown of the current NY income tax brackets for single filers:

Read also:The Ultimate Guide To Best Raspberry Pi Remoteiot Solutions For Your Smart Projects

- 4% on income up to $8,500

- 4.5% on income between $8,501 and $11,700

- 5.25% on income between $11,701 and $25,000

- 5.97% on income between $25,001 and $200,000

- 6.84% on income between $200,001 and $1,077,550

- 8.82% on income over $1,077,551

Exploring NY Income Tax Deductions and Credits

Beyond the basic tax brackets, NY income tax offers a range of deductions and credits to help taxpayers reduce their overall liability. These benefits are designed to provide financial relief to specific groups, such as low-income families, students, and retirees. For instance, the Earned Income Tax Credit (EITC) is available to working individuals and families with modest incomes, potentially resulting in a significant tax refund.

Another valuable deduction is the New York State Child Care Credit, which assists parents with the costs of childcare expenses. This credit is particularly beneficial for working families who rely on external childcare services to balance work and family responsibilities. Additionally, New York offers a deduction for contributions to 529 college savings plans, encouraging residents to save for their children's education while reducing their taxable income.

Retirees may also benefit from the New York State Pension and Annuity Exclusion, which allows them to exclude a portion of their retirement income from taxation. This exclusion is particularly advantageous for seniors who rely heavily on pension income and wish to preserve their savings for future needs. By taking advantage of these deductions and credits, taxpayers can significantly lower their NY income tax burden and improve their financial well-being.

How Do You File NY Income Tax?

Filing NY income tax involves several steps, beginning with gathering all necessary documentation, such as W-2 forms, 1099s, and records of deductions and credits. Once you have all the required information, you can choose to file your taxes electronically or by mail. Electronic filing is generally faster and more convenient, offering features like direct deposit for refunds and automated error detection to ensure accuracy.

When preparing your NY income tax return, it's crucial to accurately report all sources of income, including wages, self-employment earnings, investment gains, and rental income. Failure to disclose all income can result in penalties and interest charges, making it essential to maintain thorough and organized financial records throughout the year. Additionally, reviewing your tax return for errors before submission can help prevent unnecessary delays or audits.

For those who prefer professional assistance, hiring a certified tax preparer or accountant can provide peace of mind and ensure compliance with complex tax regulations. These experts can also identify potential deductions and credits you may have overlooked, potentially saving you money in the long run. Whether you file independently or seek professional help, staying informed about NY income tax requirements is key to a successful filing experience.

Why Does Local NY Income Tax Matter?

In addition to state income tax, many New York residents must contend with local income taxes imposed by their municipalities. These taxes vary widely depending on where you live, with some areas imposing no local tax while others levy rates as high as 3.648% of taxable income. For example, New York City residents face a local income tax rate that ranges from 2.907% to 3.648%, depending on their income level.

Local income taxes are typically used to fund municipal services such as public schools, police and fire departments, and road maintenance. While these services are essential for maintaining quality of life, the added tax burden can strain household budgets, especially for low- and middle-income families. Understanding your local tax obligations and how they interact with state taxes is crucial for accurate financial planning and compliance with tax laws.

Residents living in multiple jurisdictions throughout the year may also need to consider how local taxes apply to their income. For instance, individuals who work in New York City but reside in a neighboring suburb may be subject to both city and county taxes. In such cases, it's important to consult a tax professional to ensure proper allocation and avoid overpayment or underpayment of taxes.

How Can You Reduce Your NY Income Tax?

Reducing your NY income tax liability involves a combination of strategic planning, leveraging available deductions and credits, and staying informed about tax law changes. One effective method is to contribute to tax-advantaged accounts, such as 401(k) plans, IRAs, and 529 college savings plans. These contributions not only lower your taxable income but also help you build long-term financial security.

Another way to minimize your tax burden is to itemize deductions instead of taking the standard deduction. Itemizing allows you to deduct qualified expenses such as mortgage interest, property taxes, medical expenses, and charitable contributions. While this approach requires more effort and record-keeping, it can result in significant tax savings for those with substantial deductions.

Finally, staying up-to-date with changes in NY income tax laws and regulations is essential for optimizing your tax strategy. Tax laws are subject to frequent updates, and missing out on new deductions or credits could cost you money. Regularly consulting with a tax professional or using reputable tax software can help ensure you're taking full advantage of all available opportunities to reduce your tax liability.

What Impact Does NY Income Tax Have on Your Finances?

NY income tax plays a significant role in shaping your overall financial landscape, influencing everything from your disposable income to your long-term savings goals. High tax rates, particularly in urban areas like New York City, can strain household budgets and make it challenging to save for major expenses such as home purchases, education, and retirement. Understanding how much of your income is allocated to taxes is the first step in developing a comprehensive financial plan.

By incorporating tax considerations into your budgeting process, you can better anticipate your net income and plan accordingly. For example, setting aside a portion of each paycheck for taxes can help prevent surprises at tax time and ensure you have sufficient funds to cover your obligations. Additionally, exploring tax-efficient investment strategies, such as utilizing tax-deferred accounts, can enhance your savings growth over time.

Ultimately, the impact of NY income tax on your finances depends on your income level, filing status, and ability to leverage available deductions and credits. By taking a proactive approach to tax planning, you can minimize your liability and maximize your financial resources, empowering you to achieve your short- and long-term goals.

Where Is NY Income Tax Headed in the Future?

The future of NY income tax is shaped by a combination of economic factors, legislative priorities, and demographic trends. In recent years, New York has implemented several tax reforms aimed at addressing budget shortfalls and promoting economic growth. These changes include adjustments to tax brackets, increases in the standard deduction, and enhancements to existing credits and deductions.

Looking ahead, policymakers may continue to explore ways to modernize the tax code and make it more equitable for all residents. Potential reforms could include simplifying the filing process, expanding eligibility for credits and deductions, and addressing disparities in local tax rates. Additionally, as the state grapples with aging infrastructure and growing healthcare costs, there may be pressure to increase revenue through tax adjustments or new levies.

Staying informed about these developments is crucial for New Yorkers who wish to adapt their financial strategies to changing tax landscapes. By maintaining awareness of legislative updates and consulting with tax professionals, residents can ensure their plans remain aligned with evolving tax policies and maximize their financial well-being.

Frequently Asked Questions About NY Income Tax

1. Do I Need to File NY Income Tax If I Don't Live in New York?

If you earn income from sources within New York State, such as wages from a job or rental income, you may still be required to file a NY income tax return. Nonresidents who work in New York are typically subject to state income tax on their New York-sourced income, even if they reside elsewhere. It's important to consult the specific rules regarding nonresident filing requirements to ensure compliance.

2. Can I Deduct State and Local Taxes on My Federal Return?

Yes, under the Tax Cuts and Jobs Act (TCJA), taxpayers can deduct up to $10,000 in state and local taxes (SALT) on their federal income tax returns. This deduction includes property taxes, NY income tax, and certain other state and local levies. However, the $10,00