New York State income tax is one of the most significant financial obligations for residents, impacting individuals, families, and businesses alike. Whether you're a long-time resident or new to the state, understanding how this tax system works is crucial for effective financial planning. With its progressive tax rates and various deductions, New York's tax structure can seem complex at first glance. However, by breaking it down into manageable parts, you can ensure compliance while maximizing your savings. This guide aims to provide clarity and actionable insights into New York State income tax, helping you navigate its intricacies with confidence.

Living in New York comes with its own set of financial responsibilities, and state income tax plays a key role in funding essential services like education, healthcare, infrastructure, and public safety. The state government relies heavily on these revenues to maintain and improve the quality of life for all residents. As such, staying informed about tax laws and updates is not just beneficial—it's essential. From understanding tax brackets to exploring potential credits and deductions, this article delves into everything you need to know about New York State income tax.

By the end of this guide, you'll have a clear understanding of how New York State income tax works, including its rates, filing requirements, and strategies for minimizing your tax liability. Whether you're preparing for tax season or looking to enhance your financial literacy, this comprehensive resource will equip you with the knowledge you need to make informed decisions. Let's dive in!

Read also:Exploring The World Of Kannada Movierulz Kannada Your Ultimate Guide To Entertainment

Table of Contents

- What Is New York State Income Tax?

- How Does New York State Income Tax Work?

- Who Needs to Pay New York State Income Tax?

- How Much Is New York State Income Tax?

- How Can You Reduce Your New York State Income Tax Liability?

- Why Is New York State Income Tax Important?

- What Are the Common Mistakes to Avoid When Filing New York State Income Tax?

- How Can You Prepare for New York State Income Tax Season?

What Is New York State Income Tax?

New York State income tax is a mandatory tax levied on the earnings of individuals, businesses, and other entities residing or operating within the state. It serves as a critical source of revenue for the state government, funding vital public services such as schools, hospitals, roads, and emergency services. Unlike federal income tax, New York State income tax operates independently, with its own set of rules, rates, and deadlines.

This tax applies to various forms of income, including wages, salaries, tips, investment earnings, and self-employment income. Residents are required to file their state tax returns annually, typically by April 15th, coinciding with the federal tax deadline. However, it's important to note that New York State offers its own unique deductions, credits, and exemptions that can significantly impact your tax liability.

For example, residents may qualify for the New York State Earned Income Tax Credit (EITC), which provides financial relief to low- and moderate-income families. Additionally, New York offers specific deductions for contributions to retirement accounts, student loan interest, and medical expenses. Understanding these provisions can help you optimize your tax strategy and reduce your overall tax burden.

How Is New York State Income Tax Different From Federal Income Tax?

While both New York State and federal income taxes aim to generate revenue, they differ in several key ways. First, New York State income tax rates are generally lower than federal rates, but they vary depending on your income level and filing status. Second, the state offers unique deductions and credits that aren't available at the federal level, such as the New York State Child and Dependent Care Credit.

Another distinction lies in the treatment of certain types of income. For instance, New York State excludes specific retirement income from taxation, whereas federal rules may require you to report it. Furthermore, New York State allows residents to deduct their federal taxes from their state taxable income, providing an additional layer of relief.

What Are the Benefits of Paying New York State Income Tax?

Paying New York State income tax directly contributes to the well-being of the community. The funds collected support essential services that benefit everyone, from funding public schools and universities to maintaining parks and recreational facilities. Additionally, compliance with state tax laws ensures access to valuable credits and deductions, helping you save money and improve your financial health.

Read also:California Roll Cucumber Salad Recipe A Fusion Dish Thats Light And Flavorful

How Does New York State Income Tax Work?

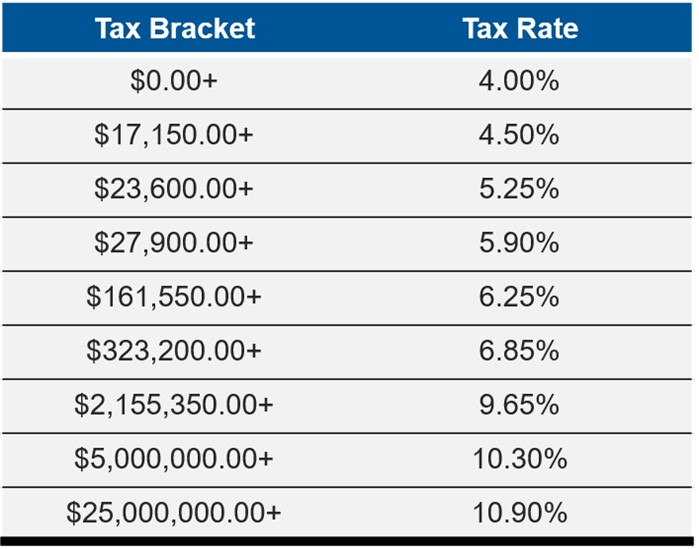

New York State income tax operates on a progressive tax system, meaning that higher income levels are subject to higher tax rates. This structure ensures that individuals and families with greater financial means contribute proportionally more to the state's revenue. The tax rates are determined based on your filing status (single, married filing jointly, etc.) and your annual income.

For example, as of the latest tax year, the lowest tax rate for New York State income tax is 4%, while the highest rate is 10.9%. These rates apply to specific income brackets, with each bracket taxed at its corresponding rate. This means that if you fall into multiple brackets, only the portion of your income within each bracket is taxed at that rate. This approach ensures fairness and prevents excessive taxation on lower-income individuals.

In addition to the base tax rates, New York State offers various deductions and credits to help reduce your taxable income. These include standard deductions, itemized deductions, and tax credits for education, child care, and energy-efficient home improvements. By taking advantage of these provisions, you can lower your overall tax liability and retain more of your hard-earned money.

How Are Tax Brackets Determined for New York State Income Tax?

Tax brackets for New York State income tax are established based on your filing status and annual income. For single filers, the brackets range from $8,500 to $215,400, with each bracket taxed at a different rate. Married couples filing jointly have higher thresholds, reflecting their combined income. For example, a married couple earning $150,000 would fall into a lower tax bracket than a single individual earning the same amount.

It's important to note that these brackets are subject to change annually, as the state adjusts them to account for inflation and other economic factors. Staying informed about these updates can help you plan effectively and avoid unexpected tax liabilities.

What Role Do Deductions Play in New York State Income Tax?

Deductions play a crucial role in reducing your taxable income, thereby lowering your New York State income tax liability. Standard deductions provide a fixed amount that all taxpayers can claim, while itemized deductions allow you to deduct specific expenses such as mortgage interest, property taxes, and charitable contributions. Choosing the right deduction strategy depends on your individual financial situation and the types of expenses you incur throughout the year.

Who Needs to Pay New York State Income Tax?

Not everyone residing in New York State is required to pay income tax. Generally, individuals who earn above a certain threshold or have specific types of income must file and pay taxes. This includes residents, nonresidents who work in the state, and part-year residents who live in New York for part of the year.

For example, if you're a full-time resident of New York and earn wages from employment, you're required to file a state tax return. Similarly, if you're a nonresident but work in New York, you may need to pay taxes on the income earned within the state. Part-year residents, on the other hand, must allocate their income between New York and their other state of residence based on the portion of the year spent in each location.

Exceptions to these rules include individuals with low income levels, retirees receiving certain types of pension income, and those earning only exempt forms of income, such as Social Security benefits. However, even if you're not required to file, it may still be beneficial to do so to claim any available refunds or credits.

Do Nonresidents Have to Pay New York State Income Tax?

Yes, nonresidents who work in New York State are generally required to pay income tax on the income earned within the state. This applies to individuals who commute to New York for work or perform services within the state's borders. However, nonresidents may also qualify for credits or deductions that reduce their tax liability, depending on their specific circumstances.

What Happens If You Don't Pay New York State Income Tax?

Failing to pay New York State income tax can result in serious consequences, including penalties, interest charges, and legal action. The state Department of Taxation and Finance actively enforces tax compliance, using various tools such as wage garnishments, bank account levies, and liens to collect unpaid taxes. To avoid these issues, it's essential to file your tax return on time and pay any owed amounts promptly.

How Much Is New York State Income Tax?

The amount of New York State income tax you owe depends on several factors, including your income level, filing status, and applicable deductions and credits. For most taxpayers, the tax calculation involves applying the appropriate tax rate to your taxable income after deductions. For example, if you're a single filer earning $50,000 annually, your tax liability would fall within the 6.45% tax bracket.

However, your actual tax bill may differ based on any credits or exemptions you qualify for. For instance, the New York State Child Tax Credit can reduce your liability by up to $1,000 per qualifying child, while the Mortgage Interest Deduction can significantly lower your taxable income. By carefully reviewing your financial situation and taking advantage of available provisions, you can minimize your tax burden.

How Are Tax Rates Determined for New York State Income Tax?

Tax rates for New York State income tax are established by the state legislature and are subject to periodic review and adjustment. These rates are designed to balance the need for revenue generation with the goal of promoting economic growth and stability. As such, they may fluctuate based on economic conditions, budgetary requirements, and policy priorities.

What Are the Penalties for Underpaying New York State Income Tax?

Underpaying New York State income tax can lead to penalties and interest charges, which can quickly add up over time. The state imposes a failure-to-pay penalty of 5% of the unpaid tax for each month the payment is late, up to a maximum of 25%. Additionally, interest is charged at the rate of 8% per year, compounded daily. To avoid these costs, it's important to estimate your tax liability accurately and make timely payments throughout the year.

How Can You Reduce Your New York State Income Tax Liability?

Reducing your New York State income tax liability involves a combination of strategic planning and careful execution. Start by maximizing your deductions and credits, such as the standard deduction, itemized deductions, and available tax credits. Additionally, consider contributing to tax-advantaged accounts like 401(k)s, IRAs, or health savings accounts (HSAs), which can lower your taxable income.

Another effective strategy is to time your income and deductions strategically. For example, if you anticipate a significant increase in income next year, you may want to accelerate deductions into the current year to take advantage of lower tax rates. Conversely, if you expect your income to decrease, delaying deductions until the following year could result in greater tax savings.

What Are Some Common Deductions for New York State Income Tax?

Common deductions for New York State income tax include mortgage interest, property taxes, charitable contributions, and medical expenses exceeding 7.5% of your adjusted gross income (AGI). Additionally, you can deduct contributions to qualified retirement plans, student loan interest, and certain business expenses. By itemizing these deductions, you can significantly reduce your taxable income and lower your tax bill.

How Do Tax Credits Work for New York State Income Tax?

Tax credits provide dollar-for-dollar reductions in your tax liability, making them more valuable than deductions. New York State offers a variety of credits, including the Earned Income Tax Credit, Child Tax Credit, and Mortgage Credit Certificate. To claim these credits, you must meet specific eligibility requirements and provide supporting documentation when filing your tax return.

Why Is New York State Income Tax Important?

New York State income tax plays a vital role in funding essential services that benefit all residents. From supporting public education and healthcare systems to maintaining infrastructure and ensuring public safety, the revenues generated from this tax contribute to the state's overall well-being. Paying your fair share ensures that these services remain accessible and of high quality for everyone.

Moreover, compliance with New York State income tax laws helps protect your financial interests. By staying informed about tax rules and updates, you can avoid penalties, interest charges, and legal issues. Additionally, understanding your tax obligations empowers you to make informed decisions about your finances, helping you achieve long-term stability and security.

How Does New York State Income Tax Impact Local Communities?

New York State income tax directly impacts local communities by funding programs and initiatives that improve quality of life. For instance, tax revenues support public schools, libraries, parks, and recreational facilities, providing residents with access to educational and cultural resources. They also fund emergency services, such as fire departments and police forces, ensuring the safety and security of all community members.

What Are the Economic Benefits of New York State Income Tax?

From an economic perspective, New York State income tax helps stimulate growth and development by investing in key sectors such as education, infrastructure, and healthcare. These investments create