New York tax is a complex yet crucial aspect of financial management for residents, businesses, and visitors alike. As one of the most economically vibrant states in the U.S., New York imposes various types of taxes that directly impact individuals and corporations. From income and sales tax to property and excise taxes, navigating the state's tax landscape can be overwhelming without proper guidance. This article aims to demystify the intricacies of New York tax by offering a detailed overview of its components, obligations, and strategies for compliance. Whether you're a newcomer to the state or a seasoned taxpayer, this guide will provide you with the knowledge needed to make informed financial decisions.

Taxes are not just a financial obligation but also a civic responsibility. In New York, the tax system is designed to fund public services, infrastructure, education, healthcare, and other essential programs that benefit society. However, with numerous rules, deadlines, and exemptions, staying compliant can be challenging. This article addresses the most common questions and concerns related to New York tax, offering practical advice and expert insights to help you manage your tax obligations effectively. By understanding the nuances of the state's tax structure, you'll be better equipped to plan your finances and avoid costly mistakes.

From calculating your tax liability to identifying potential deductions and credits, this guide covers everything you need to know about New York tax. Whether you're filing individually, running a small business, or managing a large corporation, the information provided here will serve as a valuable resource. Let's dive into the details and explore how you can navigate the complexities of New York's tax system while maximizing your savings and minimizing your burden.

Read also:Gong Yoo Tattoo The Full Story Behind His Ink And Its Meaning

Table of Contents

- 1. What Are the Different Types of New York Tax?

- 2. How Does New York Income Tax Work?

- 3. Sales Tax in New York: A Breakdown

- 4. Property Tax in New York: What You Need to Know

- 5. Is New York Tax Fair for Everyone?

- 6. How Can You Reduce Your New York Tax Liability?

- 7. What Are the Consequences of Not Paying New York Tax?

- 8. Frequently Asked Questions About New York Tax

What Are the Different Types of New York Tax?

New York tax encompasses a wide range of categories, each tailored to specific financial activities and obligations. Understanding these types is the first step toward effective tax management. The primary categories include income tax, sales tax, property tax, excise tax, and estate tax. Each type serves a distinct purpose and impacts different aspects of your financial life.

Income tax, for instance, is levied on the earnings of individuals and businesses. It is calculated based on your gross income, deductions, and applicable tax brackets. Sales tax, on the other hand, applies to purchases of goods and services, with rates varying by county and city. Property tax is assessed on real estate holdings, while excise tax targets specific commodities like gasoline, tobacco, and alcohol. Lastly, estate tax is imposed on the transfer of assets after death. By familiarizing yourself with these categories, you can better anticipate your tax liabilities and plan accordingly.

Here’s a quick breakdown of the key types:

- Income Tax: Based on earnings and subject to progressive rates.

- Sales Tax: Applied to retail purchases and varies by location.

- Property Tax: Assessed on real estate and depends on property value.

- Excise Tax: Levied on specific goods and services.

- Estate Tax: Imposed on inherited assets exceeding a certain threshold.

Understanding the interplay between these tax types is essential for optimizing your financial strategy. For example, homeowners may benefit from property tax exemptions, while small business owners might explore deductions to reduce their income tax burden. Staying informed about each type of New York tax empowers you to make smarter financial decisions.

How Does New York Income Tax Work?

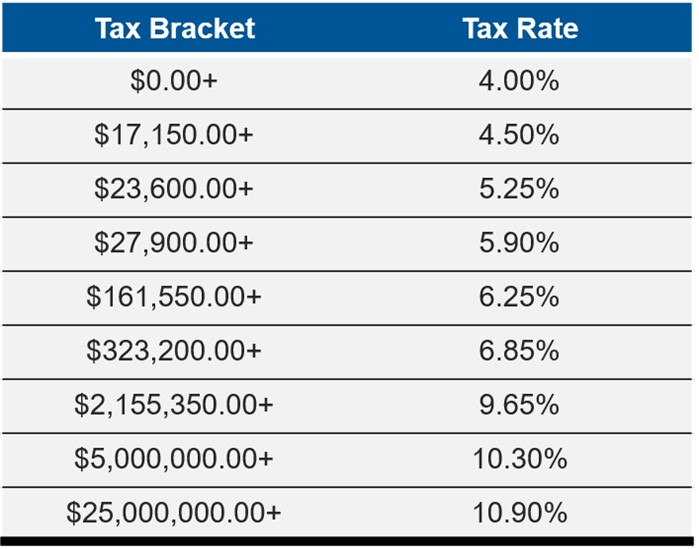

New York income tax operates on a progressive scale, meaning higher earners pay a larger percentage of their income in taxes. The state uses specific tax brackets to determine how much you owe, with rates ranging from 4% to 10.9% for the 2023 tax year. These brackets are adjusted annually to account for inflation and economic changes.

For individuals, gross income includes wages, salaries, tips, investment returns, and other forms of earnings. Deductions and credits can significantly lower your taxable income, making it crucial to understand which ones apply to your situation. Common deductions include contributions to retirement accounts, mortgage interest, and educational expenses. Credits, such as the Child Tax Credit or Earned Income Tax Credit, offer dollar-for-dollar reductions in your tax liability.

Read also:Mastering Remoteiot Vpc Ssh Windows 10 A Comprehensive Guide

Businesses in New York also face income tax obligations, with rates depending on their structure and revenue. Corporations pay a flat rate of 6.5%, while partnerships and sole proprietorships pass through their income to the owners, who then report it on their personal returns. Proper record-keeping and consultation with a tax professional are essential for ensuring compliance and maximizing savings.

Sales Tax in New York: A Breakdown

Sales tax in New York is a critical revenue source for the state, counties, and municipalities. The statewide sales tax rate is 4%, but additional local rates can push the total as high as 9.875% in certain areas. These variations mean that the cost of goods and services can differ significantly depending on where you shop.

Not all purchases are subject to sales tax, however. Exemptions exist for items like food purchased for home consumption, prescription medications, and some clothing priced under $110. Additionally, certain holidays or events may offer temporary tax exemptions, providing an opportunity for savings. It's important to stay updated on these rules, as they can change frequently.

Businesses collecting sales tax must remit the funds to the state regularly, typically monthly or quarterly. Failure to comply can result in penalties and interest charges. By understanding the nuances of New York sales tax, consumers and businesses alike can better manage their finances and avoid unexpected costs.

Property Tax in New York: What You Need to Know

Property tax is a significant expense for homeowners and commercial property owners in New York. Unlike income and sales tax, property tax is based on the assessed value of your property rather than your earnings or spending habits. The assessment process involves evaluating factors like location, size, age, and condition of the property to determine its taxable value.

Each county and municipality sets its own property tax rates, leading to wide variations across the state. For example, suburban areas with high property values often have higher tax bills than rural regions. Homeowners can apply for exemptions or reductions, such as the School Tax Relief (STAR) program, which offers savings for primary residences. Senior citizens and veterans may also qualify for additional breaks.

Paying property tax on time is essential to avoid penalties and potential legal issues. Many counties offer installment plans to ease the burden, allowing property owners to spread payments throughout the year. Staying informed about your rights and responsibilities as a property owner is key to maintaining financial stability and protecting your investment.

Is New York Tax Fair for Everyone?

The fairness of New York tax is a topic of ongoing debate among policymakers, economists, and taxpayers. Critics argue that the current system disproportionately affects low- and middle-income individuals, who may struggle to meet their obligations while wealthier residents benefit from loopholes and deductions. Proponents, however, emphasize the importance of funding vital public services and maintaining a balanced budget.

Progressive income tax brackets aim to address income inequality by requiring higher earners to contribute more. However, the complexity of the tax code and the availability of credits and exemptions can create disparities in how much people pay relative to their means. Additionally, the burden of sales and property tax can feel regressive, as they take a larger percentage of income from those with lower earnings.

Efforts to reform the tax system are ongoing, with proposals ranging from simplifying the code to introducing new taxes on luxury goods or financial transactions. While no system is perfect, continuous evaluation and adjustment are necessary to ensure that New York tax remains fair and equitable for all residents.

How Can You Reduce Your New York Tax Liability?

Reducing your New York tax liability involves a combination of strategic planning and proactive measures. One of the most effective ways is to take advantage of available deductions and credits. For income tax, this might include contributing to a retirement account, claiming dependent exemptions, or itemizing deductions for medical expenses, charitable contributions, and state taxes paid.

For businesses, optimizing expenses and timing income can help minimize taxable profits. Investing in equipment or technology that qualifies for tax incentives, such as energy-efficient upgrades, can also lead to savings. Keeping meticulous records of all transactions and consulting with a tax advisor ensures that you don't miss any opportunities.

Property owners can challenge their assessments if they believe the value assigned to their property is inaccurate. This process requires gathering evidence and presenting it to the local board of assessors, but successful appeals can result in lower tax bills. By staying informed about the latest tax laws and leveraging available resources, you can effectively reduce your New York tax burden.

What Are the Consequences of Not Paying New York Tax?

Failure to pay New York tax on time can lead to severe consequences, including penalties, interest charges, and legal action. The state takes tax compliance seriously and has mechanisms in place to enforce collection efforts. For individuals, unpaid taxes can result in wage garnishment, bank account levies, or the seizure of assets. Businesses may face additional repercussions, such as revocation of licenses or closure.

Interest accrues on overdue balances at a rate set by the state, compounding the initial debt over time. Penalties can range from a flat fee to a percentage of the unpaid amount, depending on the severity of the infraction. In extreme cases, the New York State Department of Taxation and Finance may pursue criminal charges against delinquent taxpayers.

Addressing tax issues promptly is crucial to avoiding these outcomes. If you're unable to pay your full tax liability, consider entering into an installment agreement or applying for an abatement. Communicating with the authorities and demonstrating a willingness to resolve the matter can often mitigate the consequences and provide a pathway to compliance.

Why Is Understanding New York Tax Important for Businesses?

For businesses operating in New York, understanding the tax landscape is vital for long-term success. Compliance with state regulations ensures that you avoid penalties and maintain a positive reputation with customers and partners. Moreover, leveraging available deductions and credits can enhance profitability and competitiveness.

Businesses must navigate various tax obligations, including payroll taxes, sales tax, and corporate income tax. Each requires accurate reporting and timely payment, making robust accounting systems and knowledgeable personnel essential. Outsourcing tax management to professionals or using specialized software can further streamline operations and reduce the risk of errors.

Staying informed about legislative changes and economic trends also helps businesses adapt to new challenges and opportunities. By prioritizing tax education and planning, entrepreneurs can position themselves for sustained growth and stability in the dynamic New York market.

Can New York Tax Be Simplified for Taxpayers?

Simplifying New York tax is a goal shared by many stakeholders, including lawmakers, advocacy groups, and taxpayers themselves. Streamlining the process involves reducing complexity, eliminating redundant requirements, and enhancing accessibility to resources. Efforts to digitize tax filing and payment systems have already improved convenience, but further improvements are needed to address lingering issues.

One potential solution is the adoption of uniform standards across counties and municipalities, minimizing discrepancies in tax rates and rules. Simplified forms and clearer instructions could also reduce confusion and errors. Additionally, increasing public awareness about available resources, such as free filing services and tax assistance programs, can empower taxpayers to navigate the system more effectively.

While complete simplification may not be achievable due to the state's diverse needs and priorities, incremental changes can significantly enhance the taxpayer experience. Continued collaboration between government agencies and community organizations is essential to driving progress in this area.

Frequently Asked Questions About New York Tax

1. How Do I File My New York Tax Return?

Filing your New York tax return involves gathering necessary documents, completing the appropriate forms, and submitting them by the deadline. Most taxpayers use the state's online filing system, which offers convenience and faster processing times. You'll need your W-2s, 1099s, and other income-related documents, as well as records of any deductions or credits you plan to claim.

Ensure that all information is accurate and matches what you reported on your federal return. If you owe taxes, pay them electronically or mail a check with your return. Extensions are available if you need more time to file, but any owed taxes must still be paid by the original deadline to avoid penalties.

2. What Happens If I Miss the New York Tax Deadline?

Missing the New York tax deadline can result in penalties and interest on any unpaid taxes. The state imposes a late filing penalty of 5% of the unpaid tax per month, up to a maximum of 25%. Additionally, a late payment penalty of 0.5% per month applies to the amount owed. Interest accrues at the rate set by the state, compounding the total owed over time.

If you're unable to meet the deadline, file for an extension to avoid the late filing penalty. However, any taxes due must still be paid by the original deadline. In cases of