New York taxes are a critical aspect of financial planning for both individuals and businesses. As one of the most economically vibrant states in the U.S., New York imposes a variety of tax obligations that can significantly impact residents' financial health. Whether you're a newly relocated resident, a small business owner, or a seasoned taxpayer, understanding the intricacies of New York's tax system is essential. From income taxes to sales taxes, property taxes, and beyond, the state's tax structure is designed to fund essential services while ensuring fiscal responsibility. In this article, we'll delve into the complexities of New York taxes, offering actionable insights and strategies to help you navigate the system effectively.

For many, navigating New York taxes can feel overwhelming. The state's tax codes are extensive, with numerous regulations and exemptions that vary depending on your income level, location, and type of business. Moreover, recent legislative changes have introduced new considerations that taxpayers must be aware of. Staying informed about these developments is crucial to avoiding penalties and optimizing your tax liabilities. This guide will provide a detailed overview of the key components of New York's tax system, ensuring you're well-prepared to manage your financial obligations.

Our goal is to simplify the complexities of New York taxes, offering practical advice and expert insights. By the end of this article, you'll have a comprehensive understanding of how the state's tax system works, the various types of taxes you may encounter, and strategies to minimize your tax burden. Whether you're looking to file your taxes efficiently or seeking advice on tax planning, this resource is designed to empower you with the knowledge you need to succeed. Let's dive in and explore the world of New York taxes together.

Read also:Unlocking The Potential Of Sone436 A Comprehensive Guide For The Future

Table of Contents

- 1. What Are the Key Components of New York Taxes?

- 2. How Do New York Income Taxes Work?

- 3. How Much Are Property Taxes in New York?

- 4. What Are the Sales Taxes in New York?

- 5. Exploring Business Taxes in New York

- 6. Can You Deduct New York Taxes on Your Federal Return?

- 7. Tips for Managing New York Taxes Efficiently

- 8. Frequently Asked Questions About New York Taxes

What Are the Key Components of New York Taxes?

New York taxes encompass a wide range of obligations designed to fund state and local services. These include income taxes, property taxes, sales taxes, and various other levies that impact both individuals and businesses. Understanding the key components of New York's tax system is the first step toward effective financial planning. For instance, income taxes are progressive, meaning higher earners pay a larger percentage of their income. Property taxes, on the other hand, vary significantly depending on the location and value of your property. Sales taxes also differ across counties, with additional local taxes layered on top of the state rate.

In addition to these primary taxes, New York imposes excise taxes on specific goods like gasoline, cigarettes, and alcohol. These taxes are often overlooked but can add up over time. For businesses, there are additional considerations such as corporate income taxes, franchise taxes, and payroll taxes. Each of these components plays a vital role in funding public services, infrastructure, and education, making it essential for taxpayers to understand their obligations fully.

To illustrate the complexity of New York taxes, consider the following example: a homeowner in Manhattan may face significantly higher property taxes compared to someone in upstate New York due to differences in property values and local tax rates. Similarly, a business operating in New York City might incur additional local taxes that don't apply to businesses in other parts of the state. By breaking down each component, we can better understand how these taxes affect our daily lives and financial well-being.

How Do New York Income Taxes Work?

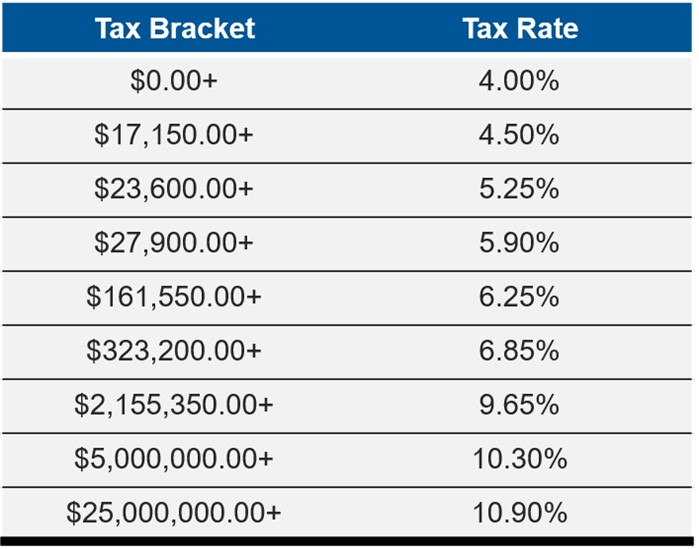

New York income taxes are structured as a progressive tax system, meaning the tax rate increases as your income rises. For the 2023 tax year, the state imposes seven tax brackets, ranging from 4% for lower-income individuals to 10.9% for those earning over $1 million annually. This system ensures that higher earners contribute a larger share of their income, promoting fiscal equity across the state. Additionally, New York offers various deductions and credits to help taxpayers reduce their liabilities.

For example, the state provides an Earned Income Tax Credit (EITC) for low- and moderate-income workers, which can significantly lower your tax burden. There are also exemptions for certain types of income, such as Social Security benefits and military pensions. Understanding these deductions and credits is crucial for maximizing your tax savings. Furthermore, New York residents must file both state and federal income tax returns, ensuring compliance with all applicable regulations.

It's important to note that New York City imposes its own income tax, adding another layer of complexity for residents. The city tax rates range from 2.906% to 3.876%, depending on your income level. This additional tax obligation underscores the importance of careful financial planning and accurate record-keeping. By staying informed about the intricacies of New York income taxes, you can ensure compliance while minimizing your overall tax burden.

Read also:Unveiling The Allure Of Lara Rose Erome A Rising Star In The Spotlight

How Much Are Property Taxes in New York?

Property taxes in New York vary widely depending on the location and assessed value of your property. On average, New York's property tax rates are among the highest in the nation, with some counties exceeding 2% of the property's assessed value. For instance, Westchester County has some of the highest property tax rates in the state, while rural areas like Hamilton County tend to have lower rates. These variations highlight the importance of understanding local tax policies when purchasing or owning property in New York.

In addition to the base tax rate, homeowners may face additional assessments for services like schools, water districts, and fire districts. These assessments can significantly increase your overall tax burden, making it essential to research local tax practices before making real estate decisions. Fortunately, New York offers several property tax relief programs, including the School Tax Relief (STAR) program and the Enhanced STAR program for seniors. These programs can provide substantial savings, helping homeowners manage their financial obligations more effectively.

What Are the Sales Taxes in New York?

Sales taxes in New York consist of a state tax rate of 4%, with additional local taxes varying by county. For example, New York City imposes a local sales tax rate of 4.457%, bringing the total sales tax rate to 8.457%. Other counties, such as Nassau and Suffolk, have slightly different rates, reflecting local government needs and priorities. Understanding these variations is crucial for businesses and consumers alike, as they can impact purchasing decisions and budgeting.

It's worth noting that certain items are exempt from sales taxes in New York, including most food items, prescription medications, and clothing and footwear costing less than $110. These exemptions help reduce the financial burden on consumers, especially for essential goods. Additionally, New York offers periodic sales tax holidays, during which specific items like clothing and school supplies are exempt from sales taxes. These holidays provide an opportunity for consumers to save money on purchases while supporting local businesses.

Exploring Business Taxes in New York

New York imposes several types of business taxes, including corporate income taxes, franchise taxes, and payroll taxes. Corporate income taxes are levied on the net income of businesses operating within the state, with rates ranging from 6.5% to 7.25% depending on the size and type of business. Franchise taxes, on the other hand, are based on the value of a corporation's capital stock and are designed to ensure fair competition among businesses.

Payroll taxes in New York include unemployment insurance contributions and workers' compensation premiums, which are calculated based on the number of employees and their wages. Businesses must also comply with federal payroll tax requirements, adding another layer of complexity to their tax obligations. By understanding these various taxes and leveraging available deductions and credits, businesses can optimize their financial performance while remaining compliant with state regulations.

Can You Deduct New York Taxes on Your Federal Return?

Yes, under the Tax Cuts and Jobs Act (TCJA), taxpayers can deduct up to $10,000 in state and local taxes (SALT) on their federal tax returns. This deduction includes property taxes, income taxes, and sales taxes paid during the tax year. For many New York residents, this cap can be a significant limitation, given the state's high tax rates. However, careful planning can help maximize your deduction and minimize your overall tax burden.

For example, if you itemize deductions on your federal return, you can choose to deduct either state income taxes or sales taxes, whichever is more beneficial. Additionally, timing your tax payments strategically can help you maximize your SALT deduction. By coordinating with a tax professional, you can ensure compliance with all federal and state regulations while optimizing your tax savings.

Tips for Managing New York Taxes Efficiently

Managing New York taxes efficiently requires a combination of careful planning, accurate record-keeping, and strategic decision-making. Start by familiarizing yourself with the state's tax codes and any recent legislative changes that may affect your obligations. Utilize available resources, such as the New York State Department of Taxation and Finance website, to stay informed about tax deadlines and requirements.

Consider the following tips for managing your taxes more effectively:

- Keep detailed records of all income, expenses, and tax payments throughout the year.

- Take advantage of available deductions and credits to reduce your tax liabilities.

- Consult with a tax professional to ensure compliance and optimize your tax strategy.

- Plan ahead for tax payments, especially if you're self-employed or own a business.

- Stay informed about changes in tax laws that may impact your obligations.

Frequently Asked Questions About New York Taxes

1. Do I Have to Pay New York Taxes if I Work Remotely?

If you work remotely for a New York-based employer, you may still be required to pay New York state income taxes, depending on where you physically perform your work. Under the "convenience of the employer" rule, you're considered to be working in New York unless your employer requires you to work from another location. This rule has sparked controversy during the pandemic, as many workers shifted to remote work arrangements. Consulting with a tax professional can help clarify your obligations in this scenario.

2. Can I Appeal My Property Tax Assessment in New York?

Yes, you can appeal your property tax assessment in New York if you believe it's inaccurate or unfair. The process varies by county but typically involves filing a complaint with the local board of assessment review. Be sure to gather supporting documentation, such as comparable property assessments and recent sales data, to strengthen your case. Appealing your assessment can lead to significant tax savings, making it a worthwhile endeavor for many homeowners.

3. Are There Any Tax Incentives for Businesses in New York?

New York offers several tax incentives designed to attract and support businesses, including tax credits for job creation, research and development, and renewable energy projects. The Excelsior Jobs Program, for example, provides tax credits to businesses that create new jobs or invest in capital projects. Additionally, the Start-Up NY program offers tax-free opportunities for businesses locating near eligible university campuses. Exploring these incentives can help businesses reduce their tax liabilities while contributing to economic growth in the state.

In conclusion, New York taxes are a complex but manageable aspect of financial life for residents and businesses alike. By understanding the key components of the state's tax system and leveraging available resources, you can navigate your obligations effectively and optimize your financial well-being. Stay informed, plan ahead, and seek professional guidance when needed to ensure compliance and success in the ever-evolving world of New York taxes.