New York State taxes are a critical aspect of financial planning for residents, impacting everything from income and property to sales and excise duties. As one of the highest-tax states in the nation, New York imposes a complex web of levies designed to fund essential public services and infrastructure. From state income tax rates that vary based on income brackets to the intricacies of property tax assessments, understanding these obligations is vital for both individuals and businesses. Whether you're a long-time resident or a newcomer to the Empire State, staying informed about how these taxes work can help you make smarter financial decisions and avoid costly mistakes.

Taxes in New York State are not just a fiscal responsibility but also a reflection of the state's commitment to maintaining its status as a global economic hub. The tax system is designed to generate revenue for critical areas such as education, healthcare, transportation, and public safety. However, navigating this system can be challenging, especially for those unfamiliar with its nuances. This article aims to demystify New York State taxes by providing a detailed breakdown of the various types of taxes, key deadlines, exemptions, and strategies for minimizing your tax burden. Whether you're filing as an individual or managing a business, the information here will equip you with the knowledge you need to navigate the complexities of New York's tax landscape.

As we delve deeper into the world of New York State taxes, it's important to recognize the role they play in shaping the state's economic environment. For many residents, understanding how these taxes affect their day-to-day lives is essential for financial planning and long-term stability. This guide will explore everything from income tax brackets to sales tax rates, offering practical advice and insights to help you stay compliant and optimize your tax strategy. Let's get started by examining the various components of New York's tax system and how they impact residents across the state.

Read also:Exploring The World Of New Kannada Movierulz A Comprehensive Guide For Fans

What Are the Different Types of New York State Taxes?

New York State imposes several types of taxes that collectively contribute to the state's revenue. These include income tax, property tax, sales tax, corporate tax, and excise tax, among others. Each tax type serves a specific purpose and is calculated differently, depending on factors such as income level, property value, or the nature of the transaction. For instance, income tax is levied on the earnings of individuals and businesses, while property tax is based on the assessed value of real estate. Understanding these distinctions is crucial for residents seeking to manage their financial obligations effectively.

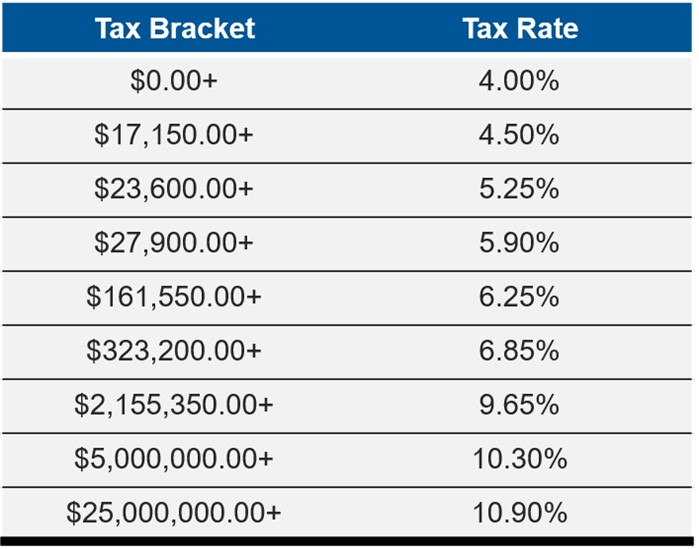

Income tax is one of the most significant components of New York State taxes, with rates that vary depending on taxable income. As of the latest tax year, the state income tax rates range from 4% to 10.9%, with higher rates applying to higher income brackets. This progressive system ensures that those earning more contribute a larger share of their income to support public services. Property tax, on the other hand, is determined by local governments and can vary significantly across counties and municipalities. Homeowners are particularly affected by these taxes, as they directly impact monthly mortgage payments and overall housing affordability.

Sales tax is another critical element of New York State taxes, affecting every purchase made within the state. The standard sales tax rate is 4%, but localities can add additional surcharges, bringing the total rate as high as 9% in some areas. Certain items, such as groceries and prescription medications, are exempt from sales tax, providing relief to consumers. Corporate taxes and excise taxes further contribute to the state's revenue, targeting businesses and specific goods or services. By exploring each of these tax types in detail, we can better understand their implications for residents and businesses alike.

How Do New York State Income Taxes Work?

New York State income taxes are calculated based on a progressive tax system, where higher income levels are subject to higher tax rates. This approach ensures that the tax burden is distributed fairly across all income groups. Residents must file their state income tax returns annually, typically by April 15th, unless extensions are granted. The process involves reporting all sources of income, including wages, investments, and self-employment earnings, and applying any applicable deductions and credits.

One of the key features of New York State income taxes is the ability to claim deductions and credits that can reduce your taxable income. For example, the New York State Earned Income Tax Credit (EITC) provides relief to low- and moderate-income families by offering a refundable credit based on federal EITC eligibility. Additionally, residents can take advantage of deductions for contributions to retirement accounts, student loan interest, and certain business expenses. These provisions aim to alleviate the financial strain on taxpayers and promote economic stability within the state.

What Are the Key Deadlines for Filing New York State Taxes?

Filing New York State taxes requires careful attention to deadlines to avoid penalties and interest. The primary deadline for submitting state income tax returns is April 15th, aligning with the federal tax deadline. However, taxpayers who need more time to prepare their returns can request an extension by filing Form IT-200. It's important to note that while an extension grants additional time to file, it does not extend the payment deadline for any taxes owed. Therefore, it's crucial to estimate and pay any outstanding amounts by the original due date to avoid late payment penalties.

Read also:How Safe Is Ullu Webseries Download Movierulz In 2023

In addition to income tax deadlines, residents must also be mindful of property tax payment schedules, which vary by locality. Most counties in New York require property taxes to be paid semi-annually, with payments due in the summer and winter. Failure to meet these deadlines can result in interest charges and, in severe cases, property liens or foreclosures. Staying organized and keeping track of all tax-related deadlines is essential for maintaining compliance and avoiding unnecessary financial burdens.

What Are the Property Tax Rates in New York State?

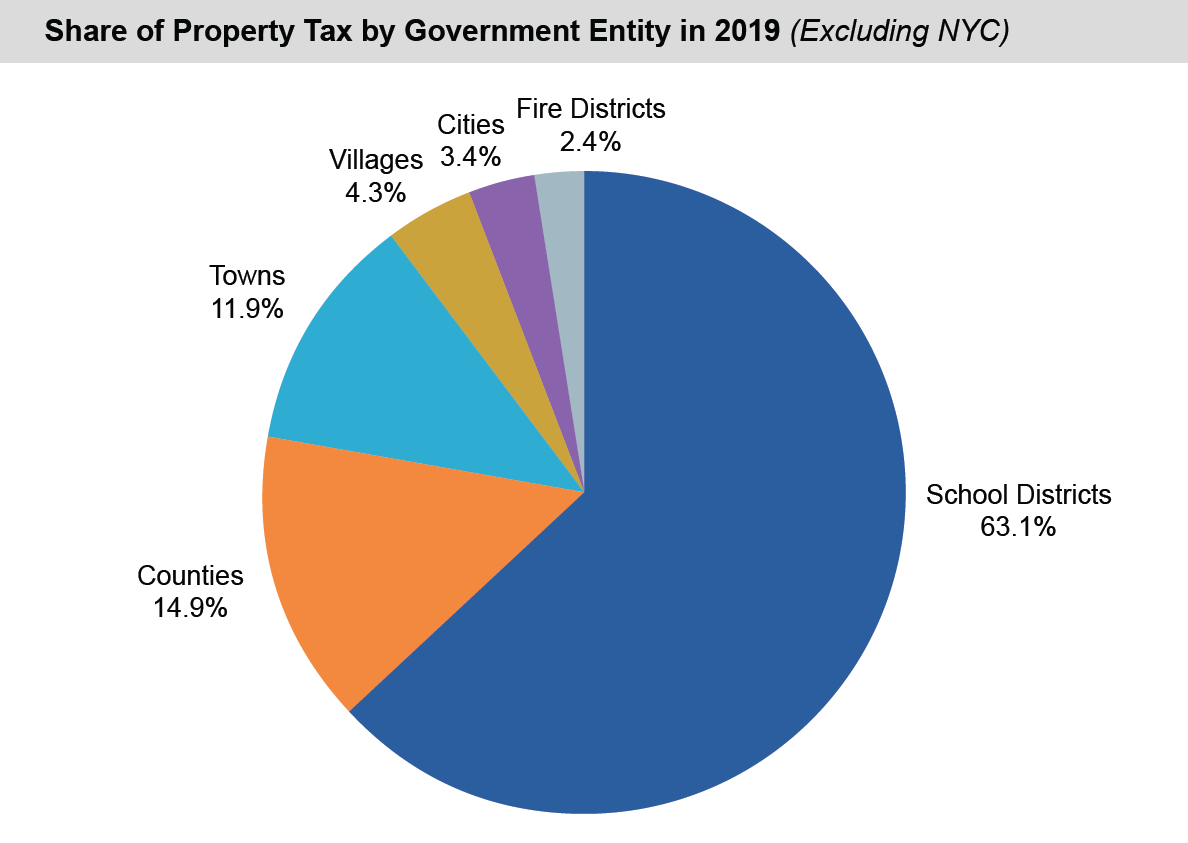

Property tax rates in New York State are determined at the local level, with each municipality setting its own assessment practices and millage rates. These rates are based on the assessed value of a property, which is typically a percentage of its market value. While the state does not impose a uniform property tax rate, it does provide guidelines and oversight to ensure fairness and consistency across jurisdictions. As a result, property tax rates can vary widely, with some areas charging significantly higher rates than others.

Homeowners in New York State can benefit from various exemptions and abatements designed to reduce their property tax burden. For example, the School Tax Relief (STAR) program offers property tax reductions to eligible homeowners, either as a basic or enhanced benefit. Additionally, senior citizens and disabled veterans may qualify for additional exemptions that further lower their tax obligations. Understanding these options and applying for them promptly can help homeowners save money and maintain financial stability.

How Can Residents Lower Their Property Tax Bills?

Lowering property tax bills in New York State often requires a proactive approach, starting with a thorough review of the property's assessed value. If you believe your assessment is inaccurate or inflated, you can file an appeal with your local assessment office. This process involves presenting evidence to support your claim, such as recent property sales in your area or improvements made to neighboring homes. In some cases, hiring a professional tax consultant can improve your chances of success and ensure that your appeal is handled efficiently.

Beyond appeals, residents can explore other strategies to reduce their property tax bills, such as taking advantage of available exemptions and credits. For instance, the Enhanced STAR program offers greater savings for senior homeowners with limited incomes, while the Green Property Tax Credit encourages energy-efficient home improvements. By combining these approaches, homeowners can significantly decrease their annual property tax payments and allocate those savings toward other financial priorities.

Understanding Sales Tax in New York State

Sales tax in New York State is a consumption-based tax levied on the sale of goods and services. The state sales tax rate is set at 4%, but localities can impose additional surcharges, bringing the total rate as high as 9% in some areas. These taxes are collected by retailers and remitted to the state and local governments, providing a significant source of revenue for public services and infrastructure. Consumers should be aware of the items subject to sales tax, as certain essential goods, such as groceries and prescription medications, are exempt from taxation.

In addition to the standard sales tax, New York State imposes special taxes on specific goods and services, such as alcohol, tobacco, and gasoline. These excise taxes are designed to generate additional revenue while discouraging the consumption of certain products. For example, the tax on cigarettes is among the highest in the nation, reflecting the state's commitment to reducing smoking rates and promoting public health. Understanding these additional taxes and their implications can help consumers make informed purchasing decisions and manage their budgets more effectively.

Can Businesses Deduct New York State Taxes?

Businesses operating in New York State can deduct certain taxes as part of their overall tax strategy, provided they meet specific criteria and adhere to federal guidelines. For instance, corporations can deduct state income taxes paid as a business expense on their federal tax returns. Similarly, self-employed individuals and partnerships may be eligible to deduct state and local taxes under the Tax Cuts and Jobs Act (TCJA), which limits the deduction to $10,000 annually. These provisions aim to ease the tax burden on businesses and encourage economic growth within the state.

It's important for businesses to consult with tax professionals or accountants to ensure they are maximizing their deductions and staying compliant with state and federal regulations. This involves maintaining accurate records, tracking expenses, and staying informed about any changes in tax laws or policies. By leveraging available deductions and credits, businesses can improve their financial performance and reinvest in their operations, contributing to the broader economic health of New York State.

What Are the Corporate Tax Rates in New York State?

Corporate tax rates in New York State are designed to balance the need for revenue generation with the goal of fostering a business-friendly environment. As of the latest tax year, the standard corporate tax rate is 6.5%, with additional surcharges for corporations with higher net incomes. These surcharges range from 0.5% to 3.25%, depending on the corporation's taxable income. Additionally, businesses engaged in specific industries, such as financial services, may be subject to additional taxes or fees.

To help businesses manage their tax obligations, New York State offers various incentives and credits aimed at promoting growth and innovation. For example, the Excelsior Jobs Tax Credit provides tax relief to companies that create new jobs or invest in capital projects within the state. By taking advantage of these opportunities, businesses can reduce their overall tax burden and focus on expanding their operations and creating jobs for residents.

Exploring New York State Tax Credits and Deductions

New York State offers a wide range of tax credits and deductions designed to provide relief to residents and businesses. These provisions aim to reduce the overall tax burden while encouraging specific behaviors, such as energy conservation, charitable giving, and education investment. Some of the most popular credits include the New York State Earned Income Tax Credit (EITC), the Child and Dependent Care Credit, and the Home Energy Assistance Program ( HEAP) credit. Understanding these options and applying for them correctly can result in significant savings for taxpayers.

For businesses, New York State provides incentives such as the Excelsior Jobs Tax Credit, the Brownfield Cleanup Program Tax Credit, and the Research and Development Credit. These credits are designed to encourage economic development, environmental stewardship, and technological innovation. By taking advantage of these opportunities, businesses can lower their tax liabilities and contribute to the state's economic growth. Additionally, residents and businesses can explore local tax abatements and exemptions that may further reduce their financial obligations.

How Do Tax Credits Differ from Deductions?

Tax credits and deductions are both valuable tools for reducing tax liabilities, but they function differently and offer distinct benefits. A tax credit directly reduces the amount of tax owed, dollar for dollar, making it a more impactful form of relief. For example, a $1,000 tax credit would reduce your tax bill by exactly $1,000. In contrast, a deduction reduces the amount of income subject to taxation, resulting in a smaller reduction in taxes owed based on your marginal tax rate. Understanding the difference between these two mechanisms is essential for maximizing your tax savings and optimizing your financial strategy.

Residents and businesses should carefully evaluate their eligibility for various credits and deductions, as some may be mutually exclusive or subject to income limits. Consulting with a tax professional or using tax preparation software can help ensure that you are claiming all available benefits and avoiding common pitfalls. By leveraging these tools effectively, taxpayers can achieve greater financial stability and peace of mind.

What Are the Most Commonly Missed Tax Deductions in New York State?

Many New York State residents and businesses overlook valuable tax deductions that could significantly reduce their tax liabilities. Some of the most commonly missed deductions include contributions to retirement accounts, student loan interest payments, and home office expenses for self-employed individuals. Additionally, residents may fail to claim deductions for charitable contributions, medical expenses exceeding a certain threshold, and state and local taxes paid. By staying informed about these opportunities and maintaining accurate records, taxpayers can ensure they are taking full advantage of all available deductions.

Frequently Asked Questions About New York State Taxes

Q: Can I File My New York State Taxes Online?

Yes, New York State residents can file their taxes online through the Department of Taxation and Finance's e-filing system. This convenient option allows taxpayers to submit their returns quickly and securely, reducing the risk of errors and accelerating the refund process. To file online, you'll need your Social Security number, income information, and any relevant tax documents, such as W-2s or 1099s. Many tax preparation software programs also offer integrated e-filing services, simplifying the process even further.

Q: How Do I Appeal My Property Tax Assessment?